Contributing to a 401(k) is one of the most effective ways to impact your income tax burden. For investors, business leaders, and accredited investors it also plays a vital role in long range wealth and tax planning.

What It Means to Reduce Taxable Income With a 401(k)

Reducing taxable income is one of the primary reasons investors and professionals use a 401(k). At a basic level, taxable income is the portion of earnings the IRS uses to calculate how much tax you owe each year. Certain actions can lower that number legally and strategically. Contributing to a traditional 401(k) is one of the most established methods because it shifts income out of your current tax calculation and into long term retirement savings.

For high earners, business owners, and accredited investors, this mechanism is not just about retirement. It is also a core tax planning lever that affects cash flow, marginal tax rates, and eligibility for deductions or credits.

How Traditional 401(k) Contributions Work

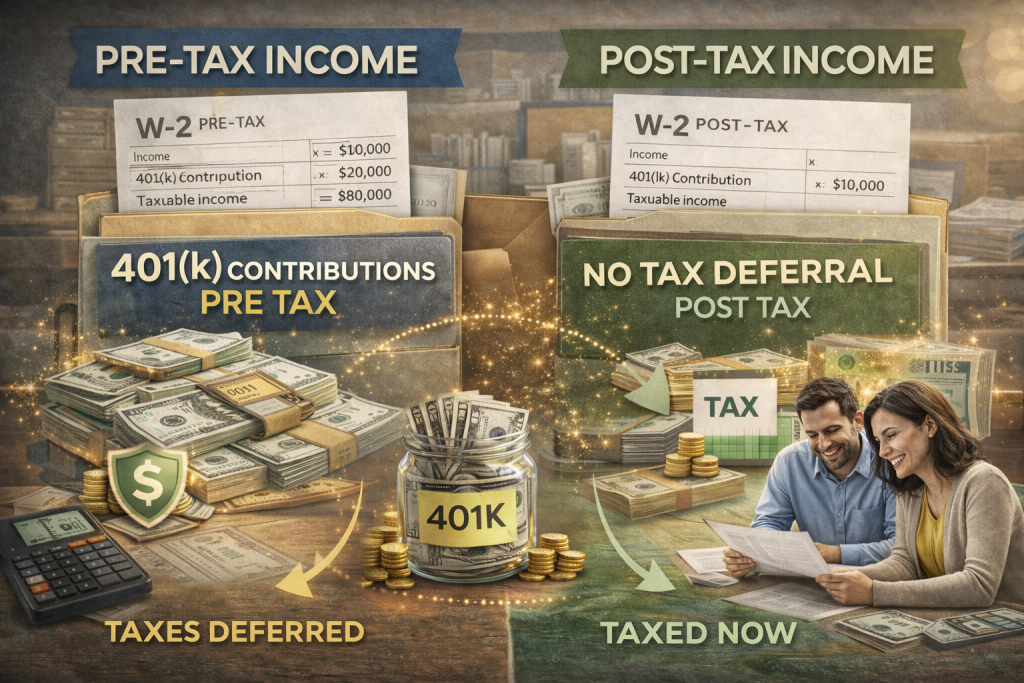

Traditional 401(k) contributions are made with pre tax dollars through payroll deferrals. This means the money is deducted from your salary before federal income taxes are calculated. As a result, the income reported on your W 2 for tax purposes is lower than your gross earnings. The IRS does not tax those deferred dollars in the year they are contributed. Instead, taxes are deferred until the funds are withdrawn in retirement. This structure allows contributors to potentially pay tax later at a lower rate. It also provides immediate tax relief in the current year, which can be especially valuable during peak earning periods.

Pre Tax Income vs Post Tax Income Defined

Pre tax income refers to earnings that have not yet been subject to income tax. Traditional 401(k) contributions fall into this category. Post tax income, on the other hand, is money that has already been taxed. Roth 401(k) contributions use post tax income, which is why they do not reduce taxable income today. The distinction matters because it determines when taxes are paid. Pre tax strategies focus on reducing current tax exposure, while post tax strategies prioritize tax free withdrawals later. Understanding this difference is essential when building a tax efficient retirement and wealth strategy.

Quantifying the Tax Impact on Federal Returns

A key step is understanding the difference between Adjusted Gross Income (AGI) and taxable income. AGI is your income after allowable adjustments. Traditional 401(k) contributions are one such adjustment.

Adjusted Gross Income (AGI) vs Taxable Income

AGI matters because it is the baseline from which your federal tax brackets and many deductions are determined.

Example: Taxable Income Reduction in Action

If you earn $150,000 and contribute $19,500 to a traditional 401(k) in 2025 your taxable income might fall to $130,500. That difference is real tax savings now.

Traditional 401(k) vs Roth 401(k) Tax Outcomes

Reducing taxable income with a 401(k) depends entirely on how contributions are treated for tax purposes. A traditional 401(k) allows eligible contributions to be deducted from income before federal taxes are calculated. A Roth 401(k) does not. This distinction matters because taxable income determines not only how much tax you owe, but also which brackets, phaseouts, and planning opportunities apply. Understanding the difference between these two structures is essential for building a tax strategy that aligns with income level, time horizon, and future expectations.

When Traditional 401(k) Makes Sense

A traditional 401(k) is most effective when the goal is to reduce current taxable income. Contributions are made with pre tax dollars, which lowers adjusted gross income and often reduces the marginal tax rate applied to remaining income.

This approach is especially valuable for higher earners, business owners, and professionals in peak earning years. Lowering taxable income can also improve eligibility for certain deductions or credits that phase out at higher income levels. The tradeoff is that withdrawals in retirement are taxed as ordinary income. For investors who expect to be in a lower tax bracket later, this deferral can produce meaningful lifetime tax savings.

When Roth 401(k) Has Strategic Value

A Roth 401(k) does not reduce taxable income in the year contributions are made. Contributions are funded with after tax dollars, which means there is no immediate tax relief. The strategic value appears later. Qualified withdrawals in retirement are tax free, including investment growth.

This structure can be attractive for younger investors, those early in their careers, or individuals who expect higher tax rates in the future. A Roth 401(k) also adds tax diversification, giving retirees flexibility in managing future taxable income. In long term planning, that flexibility can be just as important as an upfront deduction.

401(k) Tax Implications Across States and Payroll Taxes

It is important to understand that not all tax systems respond the same way.

Does 401(k) Reduce Taxable Income at the State Level?

In most states that start with your federal AGI, lowering AGI with a 401(k) also lowers state taxable income. Some states have unique treatments so always check local rules.

Payroll Tax Considerations (FICA/Medicare)

Contributions reduce income for federal and often state income tax. However they do not reduce wages subject to Social Security or Medicare withholding.

Advanced Planning: Beyond Simple Contributions

Catch-Up Contributions and High Earners

If you are over age 50 the IRS allows additional catch-up contributions. Those amounts also reduce taxable income in the year they are made.

Interaction With Other Tax Credits and Deductions

Reducing AGI with 401(k) deferrals can help you qualify for phase-outs and improved tax credit eligibility, though some credits use earned income definitions that ignore 401(k) deferrals.

Risks and Misconceptions About Taxable Income Reduction

Does Contributing Reduce Earned Income for Credits?

Not always. For certain tax credits the IRS defines earned income differently. Traditional 401(k) contributions may lower wages on a W-2 but not count as reduced earned income for specific credits.

Limits and Non-Taxable Benefits (Employer Match)

Employer matches do not count as your taxable income when made, but you are taxed on them when withdrawn in retirement.

Conclusion

Traditional 401(k) contributions do reduce taxable income today. Accredited investors and wealth strategists use this mechanism to manage tax liability and optimize long range financial outcomes. Roth plans do not offer this immediate benefit but can be powerful for tax diversification.

Continue the conversation around business growth, strategic deal-making, and intelligent capital deployment at StephenTwomey.com.