A 401K deduction refers to the portion of your wages withheld and contributed to your retirement account. For taxpayers pretax contributions lower your taxable income and create a built-in tax benefit while you save. This is fundamental for tax planning in personal finance and wealth management.

What is a 401K Deduction

A 401K deduction is payroll money you elect to direct into your retirement account before income tax is calculated. This is not a traditional itemized tax deduction you claim on Schedule A. Instead your employer reduces your taxable wages by the amount contributed. In 2025 the IRS allows up to $23,500 in elective deferrals, with higher catch-up limits for those 50 or older.

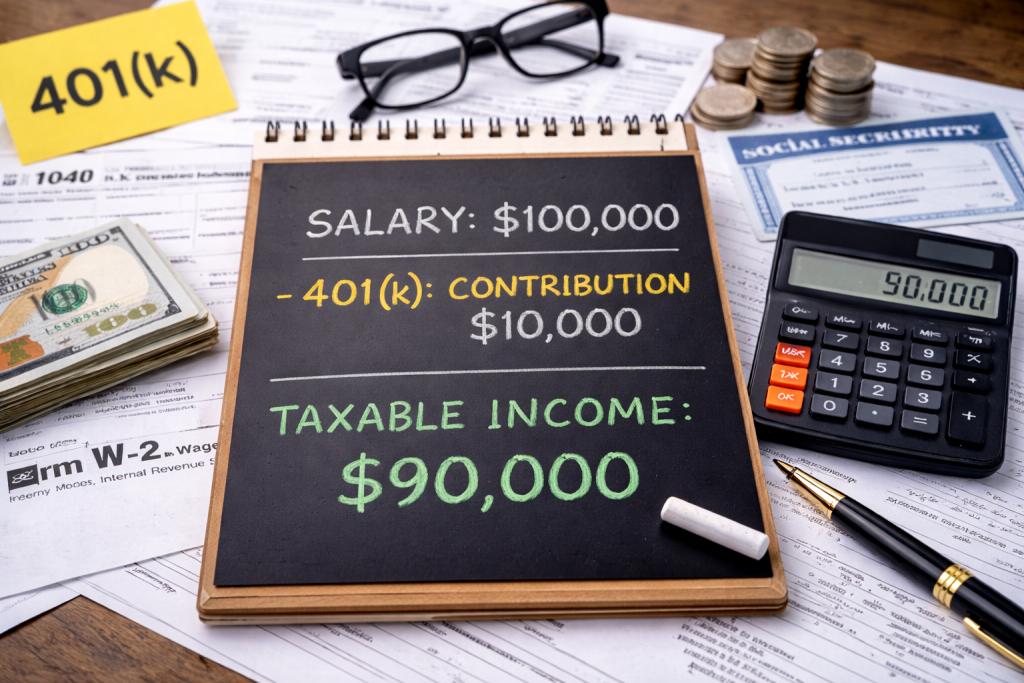

A clear example helps here. If you earn $100,000 and contribute $10,000 to a traditional 401(k) your taxable income for federal purposes becomes $90,000. This reduction can lower the tax you owe this year.

How 401(k) Contributions Affect Your Taxes

For accredited investors, a 401(k) deduction is less about basic tax savings and more about strategic income management. At higher income levels, marginal tax rates, phaseouts, and surtaxes make pretax deferrals especially valuable. A traditional 401(k) allows you to defer a portion of earned income before federal income tax is applied, effectively lowering adjusted gross income for the year. While this does not eliminate payroll taxes, it can reduce exposure to higher federal brackets and limit the impact of income-based thresholds tied to deductions and credits.

Beyond simple tax reduction, accredited investors often use 401(k) contributions as part of a broader capital allocation strategy. Lowering taxable income can improve flexibility when realizing capital gains, exercising stock options, or reallocating assets within taxable accounts.

In years with liquidity events or elevated bonus compensation, maximizing pretax contributions can smooth tax outcomes and preserve capital for alternative investments. When combined with defined benefit plans, profit sharing, or deferred compensation, the 401(k) becomes a foundational tool for long-term tax efficiency rather than a standalone retirement vehicle.

A second layer of sophistication involves timing and coordination. Accredited investors frequently face uneven income patterns tied to business exits, carried interest, or variable distributions. Strategic 401(k) contributions help offset these fluctuations and manage cash flow more predictably. While contribution limits apply, disciplined use of available deferrals can materially reduce lifetime tax drag.

Over decades, the compounding effect of tax deferral often rivals or exceeds incremental investment alpha, making the 401(k) deduction a core pillar of advanced wealth strategy rather than a basic employee benefit.

How 401(k) Contributions Affect Your Taxes

Traditional 401(k) contributions reduce taxable income at the source. Funds are withheld from payroll before federal income tax is calculated, which lowers the wages reported on your W-2. This mechanism is often misunderstood as a tax deduction claimed on a return, but the effect occurs automatically through payroll reporting. For high earners, this reduction can influence marginal tax brackets, net investment income exposure, and the effective tax rate applied to other income streams such as interest, dividends, or short-term gains.

The impact extends beyond the current tax year. By lowering adjusted gross income, 401(k) contributions can affect eligibility thresholds tied to credits, deductions, and phaseouts. While many accredited investors exceed standard limits, AGI still plays a role in Medicare premium calculations and certain surtaxes. Even small reductions can have cascading effects in years where income hovers near critical thresholds. From a planning standpoint, pretax contributions create optionality and reduce forced tax inefficiencies.

Taxes are deferred, not eliminated. Withdrawals in retirement are generally taxed as ordinary income. However, many accredited investors anticipate lower effective rates later due to reduced earned income, strategic distributions, or geographic relocation. When structured properly, deferral shifts taxation from peak earning years to periods of greater control. This timing advantage is one of the most powerful, and underappreciated, benefits of consistent 401(k) contributions within a sophisticated tax framework.

Traditional vs Roth 401(k) Tax Treatment

The distinction between traditional and Roth 401(k) contributions centers on timing. Traditional contributions reduce taxable income today and defer taxes until withdrawal. Roth contributions do not reduce current income, but qualified withdrawals are tax free. For accredited investors, the decision is rarely binary. It is a forward-looking assessment of future tax rates, liquidity needs, and portfolio composition. In high-income years, the immediate benefit of a traditional contribution often outweighs the future certainty of tax-free Roth distributions.

Traditional 401(k) accounts are often favored when current marginal rates are elevated or when income volatility is expected to decline over time. Deferring taxes during peak earning years preserves capital for reinvestment and compounds value inside a tax-deferred environment. Required minimum distributions do apply later, but careful planning can mitigate concentration risk and bracket compression. For many high earners, traditional contributions align with a strategy of deferring taxation until income becomes more discretionary.

Roth 401(k) contributions, however, serve a different purpose. They provide tax diversification and reduce future required distributions that could push retirees into higher brackets. For accredited investors with significant pretax balances, adding Roth exposure can hedge against legislative risk and rising tax rates. The optimal approach often involves blending both options across different income cycles. This creates flexibility and preserves control, which is often more valuable than optimizing for a single tax outcome.

IRS Rules and Contribution Limits (2025-2026)

The IRS updates contribution limits periodically. For 2025 the standard limit is $23,500, with catch-up contributions of $7,500 for those 50 and older. Enhanced catch-up rules may apply for ages 60–63. Total contributions including employer match generally cannot exceed $70,000.

Required Minimum Distributions start at age 73. Failure to take RMDs can trigger substantial penalties.

Employer Contributions and Tax Effect

Employer matching contributions also reduce taxable income for the employee later when distributed. For employers plan contributions can be deductible against business income subject to limits. Proper structuring of plan matches and profit sharing helps optimize both employee retirement outcomes and employer tax positions.

Advanced Tax Planning With 401(k) Strategies

Maximizing 401(k) contributions in high income years can strategically lower taxable income when it matters most. Coordinating your contributions with other retirement accounts such as IRAs or HSAs enhances overall tax efficiency.

Many tax professionals also model how 401(k) contributions affect eligibility for credits like the Saver’s Credit. Timing contributions around expected income changes can materially alter your overall tax liability.

Common Questions and Misconceptions

For accredited investors, the phrase “tax deductible” often creates confusion because 401(k) contributions do not function like itemized deductions on a tax return. Traditional 401(k) contributions are made on a pretax basis through payroll. This means the contribution reduces reported taxable wages before income tax is calculated, rather than being deducted later on Schedule A.

In practical terms, the tax benefit is real and immediate, but it occurs upstream in payroll reporting. High earners benefit most when contributions are made during peak income years, as reducing taxable wages can lower marginal tax exposure and improve overall tax efficiency.

However, these contributions are still subject to future taxation when withdrawn in retirement. For accredited investors managing multiple income streams, equity compensation, or business income, it is important to understand that a 401(k) does not eliminate taxes. It defers them. This distinction matters when modeling long term tax outcomes, liquidity needs, and retirement withdrawal strategies. The value of the deduction depends on current tax brackets versus expected future brackets, not simply on contribution size.

Do Roth 401(k) contributions reduce taxable income?

Roth 401(k) contributions do not reduce taxable income in the year they are made. Contributions are funded with after tax dollars, meaning wages are fully taxed before the contribution occurs. For accredited investors, this structure shifts the tax advantage from the present to the future.

The primary benefit of a Roth 401(k) is tax free qualified withdrawals in retirement, assuming IRS holding and age requirements are met. This can be particularly attractive for investors who expect higher tax rates later in life or who value tax diversification across retirement accounts.

While the lack of an upfront tax reduction may seem inefficient for high income earners, Roth strategies often complement traditional pretax accounts by balancing future tax exposure. Additionally, Roth 401(k) assets are increasingly used in estate planning conversations, as tax free growth can provide flexibility for heirs. The decision to use Roth contributions should be based on projected lifetime tax rates, not solely on current income levels.

Will my taxable income always decrease?

Taxable income does not always decrease simply because you contribute to a 401(k). For traditional 401(k) contributions, federal taxable income is generally reduced, but Social Security and Medicare taxes still apply to most wages. This distinction is often overlooked. As income rises beyond certain thresholds, payroll tax savings become less relevant, while income tax planning becomes more strategic. Additionally, Roth 401(k) contributions have no impact on current taxable income at all. For accredited investors with variable income, bonuses, carried interest, or business distributions, timing also matters.

A contribution may reduce taxable income in one year but create higher taxable withdrawals later, particularly when required minimum distributions begin. Changes in tax law, retirement income needs, and investment growth can all alter the long term outcome. A 401(k) is best viewed as a tax timing tool rather than a guaranteed tax reduction. Understanding how contributions interact with broader income and wealth strategies is critical for accurate planning.

For in-depth analysis on private market dynamics, business strategy, and capital formation, visit StephenTwomey.com for ongoing research and commentary.

Disclosure: None of the content in this article is financial advice.