What Is Momentum Trading?

Momentum trading is a strategy based on the idea that assets that have performed strongly recently are likely to continue performing well in the near future. Traders using momentum strategies attempt to capitalize on persistent market trends by buying rising assets and selling falling ones.

The core principle behind momentum trading is that market trends often continue longer than expected because of:

- Investor psychology

- Institutional capital flows

- Delayed information pricing

- Market inefficiencies

Momentum trading is widely used across:

- Hedge funds

- Quantitative trading firms

- Algorithmic trading systems

- Factor investing portfolios

In financial markets, momentum can exist across:

- Stocks

- Forex

- Commodities

- Cryptocurrencies

- ETFs

Many systematic quant trading strategies rely heavily on momentum factors because they have historically generated strong long-term returns across multiple asset classes.

What Is Mean Reversion Trading?

Mean reversion trading is based on the assumption that prices eventually return to their historical averages.

Rather than chasing trends, mean-reversion traders look for assets that have moved too far from normal valuation or historical behavior.

The idea is simple:

- Assets become temporarily overbought or oversold

- Market inefficiencies eventually correct themselves

- Prices revert toward equilibrium

Mean reversion strategies are extremely common in:

- Statistical arbitrage

- Quantitative hedge funds

- Market-neutral portfolios

- High-frequency trading systems

This concept forms the foundation of many statistical arbitrage strategies used by institutional quant firms.

Key Differences Between Momentum and Mean Reversion

Although both are quantitative trading approaches, momentum and mean reversion are fundamentally different in philosophy, execution, and market behavior

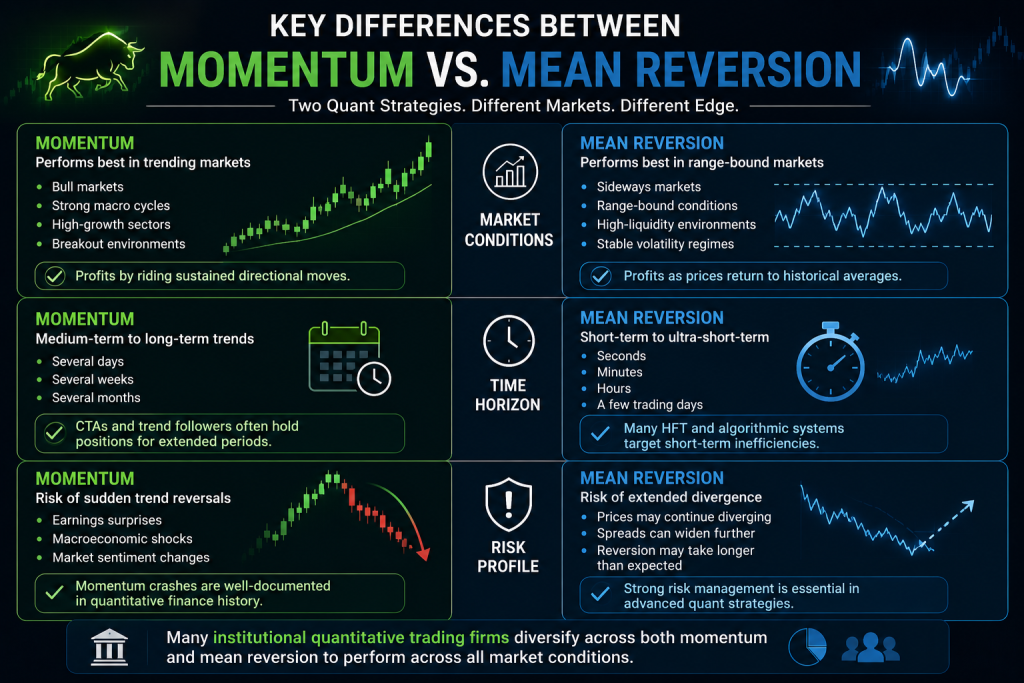

Market Conditions

Momentum strategies perform best in strongly trending markets.

Examples include:

- Bull markets

- Strong macroeconomic cycles

- High-growth sectors

- Breakout environments

Momentum traders profit by riding sustained directional moves.

In contrast, mean reversion strategies perform best in:

- Sideways markets

- Range-bound conditions

- High-liquidity environments

- Stable volatility regimes

When prices oscillate around historical averages without sustained trends, mean reversion tends to outperform.

This distinction is one reason many institutional quantitative trading firms diversify across both strategy types.

Time Horizon

Momentum trading generally operates on medium-term or long-term trends.

Holding periods may range from:

- Several days

- Several weeks

- Several months

Trend-following commodity trading advisors (CTAs) often hold positions for extended periods while trends remain intact.

Mean reversion strategies usually operate on shorter timeframes.

Holding periods can range from:

- Seconds

- Minutes

- Hours

- A few trading days

Many high-frequency algorithmic trading systems rely on ultra-short-term mean reversion opportunities.

Risk Profile

Momentum trading carries the risk of sudden trend reversals.

A strong trend can collapse quickly because of:

- Earnings surprises

- Macroeconomic shocks

- Market sentiment changes

Momentum crashes are well-documented in quantitative finance history.

Mean reversion strategies face a different problem:

- Prices may continue diverging far longer than expected

A spread that appears statistically extreme may become even more extreme before reverting.

This is one reason risk management is essential in advanced quant trading strategies.

How Momentum Trading Works

Momentum systems attempt to identify assets with strong relative strength and sustained directional movement.

Common momentum indicators include:

- Moving averages

- Relative strength index (RSI)

- MACD

- Price breakout models

Institutional momentum systems often rank thousands of securities using factor-based scoring models.

A typical momentum strategy may:

- Screen for top-performing stocks

- Rank based on recent returns

- Buy strongest assets

- Sell weakest assets

- Rebalance periodically

Momentum is one of the most researched factors in modern factor investing.

When Each Strategy Works Best

Understanding market regimes is critical because momentum and mean reversion perform differently depending on volatility and trend conditions.

Momentum Performs Best In:

- Strong bull markets

- Persistent macroeconomic trends

- Breakout environments

- Growth-driven sectors

- Trending commodity markets

Momentum thrives when investors collectively push prices in one direction for extended periods.

This is especially common during:

- Technology booms

- AI-driven rallies

- Commodity supercycles

Mean Reversion Performs Best In:

- Sideways markets

- Stable volatility periods

- High-liquidity equities

- Market-neutral environments

When prices repeatedly oscillate within ranges, mean reversion systems can consistently exploit temporary dislocations.

This is why many hedge funds combine mean reversion with algorithmic trading infrastructure.

Can You Combine Both Strategies?

Yes. Many sophisticated quant funds combine momentum and mean-reversion strategies in multi-strategy portfolios.

Firms often:

- Switch based on volatility regimes

- Use machine learning for regime detection

- Allocate dynamically between strategies

For example:

- Momentum may dominate during strong market trends

- Mean reversion may dominate during choppy or sideways conditions

Hybrid models can improve:

- Diversification

- Risk-adjusted returns

- Portfolio stability

This multi-strategy approach is common among institutional quantitative trading firms.

Real-World Examples of Momentum and Mean Reversion

Momentum Example

A trader notices Nvidia shares breaking above a major resistance level with strong volume and positive AI-related sentiment.

The trader buys the stock expecting continued momentum.

If the trend persists:

Mean Reversion Example

A pair trading system tracks Coca-Cola and Pepsi.

Historically, both stocks move closely together.

If Pepsi underperforms dramatically while Coca-Cola rallies:

- The spread widens abnormally

- The system enters a convergence trade

- The trader shorts Coca-Cola and buys Pepsi

If the spread narrows again, the trade profits.

Which Strategy Is Better for Quant Trading?

Neither strategy consistently dominates all market conditions.

Momentum tends to outperform in:

- Strong trends

- Risk-on environments

- Growth cycles

Mean reversion tends to outperform in:

- Stable markets

- Range-bound conditions

- High-liquidity environments

The best institutional systems often combine:

- Momentum

- Mean reversion

- Factor investing

- Market-neutral models

This diversification reduces dependence on any single market regime.

FAQ: Which Strategy Is More Profitable?

Neither momentum nor mean reversion is consistently more profitable across all market conditions.

Performance depends heavily on:

- Market regime

- Volatility

- Risk management

- Execution quality

- Transaction costs

Institutional investors often diversify across both approaches to improve long-term performance.

FAQ: Do Hedge Funds Use Both?

Yes. Many leading hedge funds and quantitative firms combine momentum and mean reversion within broader multi-factor portfolios.

Examples include:

- Two Sigma

- AQR Capital Management

- Renaissance Technologies

These firms combine:

- Momentum factors

- Mean reversion systems

- Statistical arbitrage

- Machine learning models

This diversified approach is common in advanced quant trading strategies.