In today’s alternative-capital environment the path to high-impact investment often runs through private market vehicles rather than public exchanges. The exemption under Rule 506(b) of Regulation D is one of the most widely used frameworks for private placements that target accredited investors and select sophisticated non-accredited investors. This article outlines how those opportunities are structured, what investors should evaluate and how to make informed decisions when engaging with 506(b) deals.

Understanding Rule 506(b) and Private Placement Basics

What is a 506(b) offering under Reg D?

A 506(b) private placement is an offering exempt from registration under the Securities Act of 1933 via Regulation D. Issuers can raise an unlimited amount of capital from unlimited accredited investors and up to 35 non-accredited but sophisticated investors.

One key constraint: no general solicitation or advertising is permitted. The offering must rely on existing relationships or direct outreach, not broadcast marketing. Eligibility of issuers and investors in a 506(b) deal

Issuers must meet standard securities-law requirements including the “bad actor” disqualification provisions. Accredited investors are individuals or entities that meet defined wealth or income thresholds (for example net worth over US$1 million excluding primary residence) or specific institutional criteria. For non-accredited participants the rule allows up to 35, provided they are “sophisticated”—in other words they have sufficient experience or access to professional advice to evaluate the investment.

Key compliance requirements — no general solicitation, Form D filing, etc.

Issuers must file Form D with the SEC within 15 days of the first sale under the exemption. If non-accredited investors participate, the issuer must provide disclosures akin to those used in registered offerings (for example audited financials, risk factors, PPM). State “blue-sky” notice filings may still apply even though federal law generally pre-empts registration.

Why 506(b) Opportunities Matter for Accredited Investors

Unlimited capital raise and broad investor access for issuers

One of the significant advantages for issuers is the ability to raise an unlimited amount of money under 506(b) while avoiding the full registration burdens of a public offering. This operational flexibility often improves deal diversity for investors by increasing supply of private placement opportunities.

The non-accredited investor allowance up to 35 participants

While many private placements restrict participation to accredited investors only, 506(b) allows up to 35 non-accredited but sophisticated investors. That feature can enable smaller investors or strategic partners to join, widening a deal’s network.

Benefits for investors: alternative asset class, diversification, deal flow

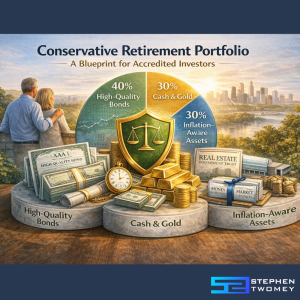

For accredited investors seeking portfolio diversification beyond public equities and debt, 506(b) offerings provide access to private capital structures—venture, private equity, real estate syndications—that are less correlated with the broader market. That can help build a more resilient portfolio in volatile environments. For example, the article on investor benefits notes:

“Alternative investments with little correlation to the public equities markets can be a good hedge against market volatility.”

Structuring and Evaluating 506(b) Deals

Private placement memorandum (PPM), disclosure and due diligence

Even though full registration is not required, issuers typically prepare a PPM that outlines the investing entity, use of proceeds, risk factors, structure of the securities, exit strategy and investor rights. From an investor’s perspective the PPM is a key document to review—check consistency, clarity and whether the terms align with market expectations.

Sponsor/issuer track record, alignment of interests and deal terms

Top-tier sponsors bring track records, clear alignment with LPs and transparent fee structures. Accredited investors should assess sponsor performance, deal terms (management fees, carried interest, hurdle rates), capital commitment by managers and governance provisions. Lack of alignment often increases risk in private placement structures.

Liquidity, exit strategy and risk considerations in 506(b) investments

501(b) securities are “restricted” which means resale is limited (often cannot be freely sold for a fixed period under Rule 144). Investors must assume that liquidity is constrained and the investment horizon is measured in years, not months. Risk factors such as sponsor execution risk, deal structure complexity, market dynamics, regulatory changes and concentration risk must be explicitly evaluated.

Comparative View — 506(b) vs 506(c)

Solicitation rules and investor verification differences

Under 506(b) general solicitation or advertising is prohibited; investors must have a pre-existing, substantive relationship with the issuer. By contrast, under Rule 506(c) advertising is permitted but all purchasers must be accredited and issuers must take reasonable steps to verify accreditation.

Use-cases for issuers and investors in each pathway

Issuers with strong networks and high-net-worth relationships often choose 506(b) to avoid verification overhead and preserve private access. 506(c) may be chosen when issuers seek broader exposure and public reach. For an accredited investor, 506(b) may bring deeper deals via a network channel; 506(c) may bring more deal flow but possibly more competition or less structural exclusivity.

Practical Checklist for Investors Exploring 506(b) Opportunities

Verify Form D filing, issuer compliance and “bad actor” status

Prior to investing, confirm via the SEC’s EDGAR system that Form D was filed within 15 days of first sale. Check whether issuers or their principals are subject to “bad actor” disqualifications under the rule.

Investor questionnaire, accreditation, sophistication and documentation

Ensure you or any non-accredited investors satisfy required sophistication certifications. Even if you are accredited, review how the issuer handles verification and investor-suitability processes. Ask for investor questionnaire templates, subscription agreement drafts, and disclosure documentation.

Strategies for monitoring and managing an illiquid private placement investment

Set expectations around communication frequency, reporting standards (e.g., quarterly investor updates, capital calls, distribution notices). From the outset, clarify exit assumptions, waterfall structure and any investor rights (e.g., major decision voting) — that positions you to manage the investment actively rather than passively.

The Future of 506(b) Private Placement Market

Trends: technology platforms, alternative asset categories, global investor reach

Recent shifts show increasing use of deal-flow platforms, digitised accreditation verification and cross-border investor access for 506(b) deals. These advances expand scale and efficiency of private placement markets. Alternative asset categories such as growth-stage technology, global real estate and private credit are increasingly being offered under 506(b) frameworks.

Regulatory and market evolution impacting 506(b) deals

Regulators continue to monitor private placement trends, particularly around investor protection, platform mediated investments and cross-border flows. Accredited investor definitions and verification processes may evolve. Staying current with regulatory commentary is critical for both issuers and investors.

Conclusion and Key Takeaways for Accredited Investors

For professional investors seeking exposure to alternative capital markets, 506(b) private placement opportunities remain a core channel. The exemption offers unlimited capital raise capability for issuers, flexible structure for investors, and a depth of deal flow that public markets cannot match. However success depends on rigorous due diligence, awareness of liquidity and structure risks, and clear alignment of interests. The difference between an average and excellent 506(b) deal often comes down to sponsor execution, transparency and investor alignment.

Disclosure: This article is for educational purposes only and does not constitute financial, legal or tax advice. Investors should consult their own professional advisors before making decisions.

In today’s alternative-capital environment the path to high-impact investment often runs through private market vehicles rather than public exchanges. The exemption under Rule 506(b) of Regulation D is one of the most widely used frameworks for private placements that target accredited investors and select sophisticated non-accredited investors. This article outlines how those opportunities are structured, what investors should evaluate and how to make informed decisions when engaging with 506(b) deals.

Understanding Rule 506(b) and Private Placement Basics

What is a 506(b) offering under Reg D?

A 506(b) private placement is an offering exempt from registration under the Securities Act of 1933 via Regulation D. Issuers can raise an unlimited amount of capital from unlimited accredited investors and up to 35 non-accredited but sophisticated investors.

One key constraint: no general solicitation or advertising is permitted. The offering must rely on existing relationships or direct outreach, not broadcast marketing. Eligibility of issuers and investors in a 506(b) deal

Issuers must meet standard securities-law requirements including the “bad actor” disqualification provisions. Accredited investors are individuals or entities that meet defined wealth or income thresholds (for example net worth over US$1 million excluding primary residence) or specific institutional criteria. For non-accredited participants the rule allows up to 35, provided they are “sophisticated”—in other words they have sufficient experience or access to professional advice to evaluate the investment.

Key compliance requirements — no general solicitation, Form D filing, etc.

Issuers must file Form D with the SEC within 15 days of the first sale under the exemption. If non-accredited investors participate, the issuer must provide disclosures akin to those used in registered offerings (for example audited financials, risk factors, PPM). State “blue-sky” notice filings may still apply even though federal law generally pre-empts registration.

Why 506(b) Opportunities Matter for Accredited Investors

Unlimited capital raise and broad investor access for issuers

One of the significant advantages for issuers is the ability to raise an unlimited amount of money under 506(b) while avoiding the full registration burdens of a public offering. This operational flexibility often improves deal diversity for investors by increasing supply of private placement opportunities.

The non-accredited investor allowance up to 35 participants

While many private placements restrict participation to accredited investors only, 506(b) allows up to 35 non-accredited but sophisticated investors. That feature can enable smaller investors or strategic partners to join, widening a deal’s network.

Benefits for investors: alternative asset class, diversification, deal flow

For accredited investors seeking portfolio diversification beyond public equities and debt, 506(b) offerings provide access to private capital structures—venture, private equity, real estate syndications—that are less correlated with the broader market. That can help build a more resilient portfolio in volatile environments. For example, the article on investor benefits notes:

“Alternative investments with little correlation to the public equities markets can be a good hedge against market volatility.”

Structuring and Evaluating 506(b) Deals

Private placement memorandum (PPM), disclosure and due diligence

Even though full registration is not required, issuers typically prepare a PPM that outlines the investing entity, use of proceeds, risk factors, structure of the securities, exit strategy and investor rights. From an investor’s perspective the PPM is a key document to review—check consistency, clarity and whether the terms align with market expectations.

Sponsor/issuer track record, alignment of interests and deal terms

Top-tier sponsors bring track records, clear alignment with LPs and transparent fee structures. Accredited investors should assess sponsor performance, deal terms (management fees, carried interest, hurdle rates), capital commitment by managers and governance provisions. Lack of alignment often increases risk in private placement structures.

Liquidity, exit strategy and risk considerations in 506(b) investments

501(b) securities are “restricted” which means resale is limited (often cannot be freely sold for a fixed period under Rule 144). Investors must assume that liquidity is constrained and the investment horizon is measured in years, not months. Risk factors such as sponsor execution risk, deal structure complexity, market dynamics, regulatory changes and concentration risk must be explicitly evaluated.

Comparative View — 506(b) vs 506(c)

Solicitation rules and investor verification differences

Under 506(b) general solicitation or advertising is prohibited; investors must have a pre-existing, substantive relationship with the issuer. By contrast, under Rule 506(c) advertising is permitted but all purchasers must be accredited and issuers must take reasonable steps to verify accreditation.

Use-cases for issuers and investors in each pathway

Issuers with strong networks and high-net-worth relationships often choose 506(b) to avoid verification overhead and preserve private access. 506(c) may be chosen when issuers seek broader exposure and public reach. For an accredited investor, 506(b) may bring deeper deals via a network channel; 506(c) may bring more deal flow but possibly more competition or less structural exclusivity.

Practical Checklist for Investors Exploring 506(b) Opportunities

Verify Form D filing, issuer compliance and “bad actor” status

Prior to investing, confirm via the SEC’s EDGAR system that Form D was filed within 15 days of first sale. Check whether issuers or their principals are subject to “bad actor” disqualifications under the rule.

Investor questionnaire, accreditation, sophistication and documentation

Ensure you or any non-accredited investors satisfy required sophistication certifications. Even if you are accredited, review how the issuer handles verification and investor-suitability processes. Ask for investor questionnaire templates, subscription agreement drafts, and disclosure documentation.

Strategies for monitoring and managing an illiquid private placement investment

Set expectations around communication frequency, reporting standards (e.g., quarterly investor updates, capital calls, distribution notices). From the outset, clarify exit assumptions, waterfall structure and any investor rights (e.g., major decision voting) — that positions you to manage the investment actively rather than passively.

The Future of 506(b) Private Placement Market

Trends: technology platforms, alternative asset categories, global investor reach

Recent shifts show increasing use of deal-flow platforms, digitised accreditation verification and cross-border investor access for 506(b) deals. These advances expand scale and efficiency of private placement markets. Alternative asset categories such as growth-stage technology, global real estate and private credit are increasingly being offered under 506(b) frameworks.

Regulatory and market evolution impacting 506(b) deals

Regulators continue to monitor private placement trends, particularly around investor protection, platform mediated investments and cross-border flows. Accredited investor definitions and verification processes may evolve. Staying current with regulatory commentary is critical for both issuers and investors.

Conclusion and Key Takeaways for Accredited Investors

For professional investors seeking exposure to alternative capital markets, 506(b) private placement opportunities remain a core channel. The exemption offers unlimited capital raise capability for issuers, flexible structure for investors, and a depth of deal flow that public markets cannot match. However success depends on rigorous due diligence, awareness of liquidity and structure risks, and clear alignment of interests. The difference between an average and excellent 506(b) deal often comes down to sponsor execution, transparency and investor alignment.

Disclosure: This article is for educational purposes only and does not constitute financial, legal or tax advice. Investors should consult their own professional advisors before making decisions.

For more insights on digital strategy, SEO and AI-driven marketing, visit StephenTwomey.com.