A conservative retirement portfolio is not just about holding bonds and cash. It is a structured plan designed to reduce large drawdowns while still supporting decades of retirement spending. For entrepreneurs and high earners, it also acts as a stabilizer against business concentration risk and unpredictable income cycles.

What is a Conservative Retirement Portfolio?

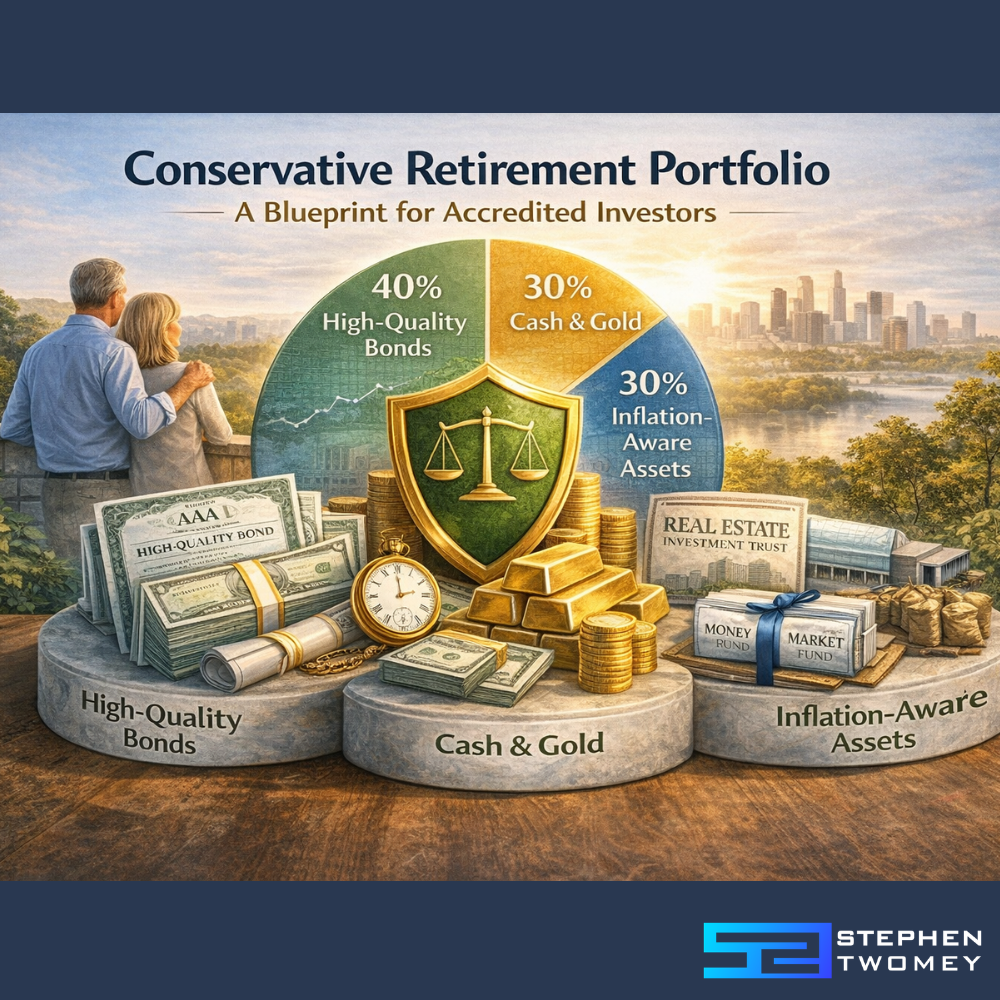

A conservative retirement portfolio is built to prioritize stability and dependable income. It typically holds a larger share of high-quality bonds, cash equivalents, and inflation-aware assets than a growth portfolio. The goal is to keep retirees invested through market cycles without being forced to sell at the wrong time.

The real definition of “conservative” in retirement

Conservative does not mean “zero volatility.” It means the portfolio is engineered to keep essential spending funded even during market stress. The best conservative portfolios reduce the chance of panic decisions by keeping enough stable assets to cover near-term withdrawals.

Quick Answer: A conservative retirement portfolio is designed to fund spending with lower volatility using a mix of bonds, cash, and a measured level of equities for inflation protection.

The two risks conservative investors underestimate

Many retirees focus only on market risk, then overcorrect into cash and short-duration bonds. That can introduce two hidden threats:

- Inflation risk: cash can lose real buying power over time.

- Longevity risk: living longer than expected requires growth, even in conservative plans.

Investopedia has recently emphasized that being “too conservative” can backfire by reducing compounding and failing to keep pace with inflation. Investopedia

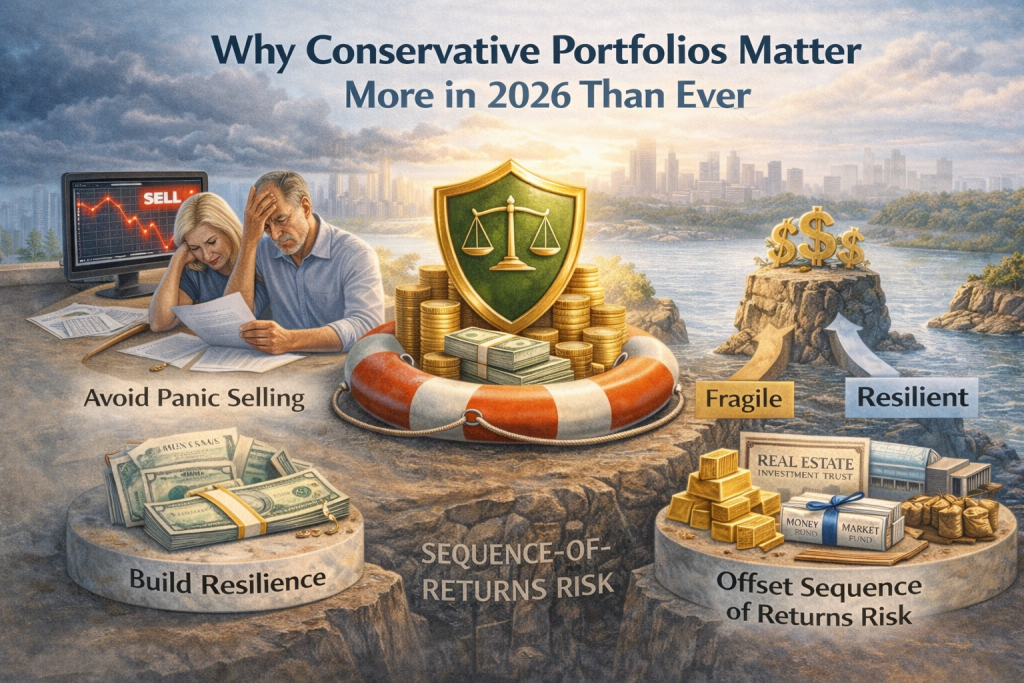

Why Conservative Portfolios Matter More in 2026 Than Ever

Markets move faster than most retirement plans. Rate cycles shift, inflation regimes change, and headlines trigger emotional decision-making. A conservative retirement portfolio matters because it reduces the need to react.

Volatility is not the enemy, panic selling is

A conservative plan is less about predicting markets and more about building a portfolio you can hold through bad periods. If your portfolio forces you to sell stocks after a downturn to pay bills, it is not conservative. It is fragile.

Sequence-of-returns risk, explained in plain English

Sequence-of-returns risk is what happens when poor market returns hit early in retirement, while you are withdrawing money. Losses early have more damage because you are pulling money out while the portfolio is down. The conservative solution is not “all bonds.” It is creating a liquidity buffer and an allocation that can recover.

Conservative Retirement Portfolio Allocations (3 Models)

There is no single correct conservative allocation. What matters is matching the allocation to spending needs, time horizon, and guaranteed income sources, a framework Schwab highlights in its retirement portfolio guidance. Schwab Brokerage

The “Income First” allocation

This model prioritizes income stability and lower drawdowns.

Example allocation:

- 50% high-quality bonds (Treasuries, investment-grade, short-to-intermediate duration)

- 20% dividend-focused equities

- 10% TIPS

- 10% CDs or money markets

- 10% cash buffer

This is similar in spirit to SmartAsset’s conservative example allocation, which emphasizes bonds, TIPS, and cash-like holdings to limit volatility. SmartAsset

Use case: Retirees who rely heavily on portfolio withdrawals for monthly expenses.

The “Inflation Defense” allocation

This model maintains more inflation awareness without taking aggressive equity risk.

Example allocation:

- 40% bonds

- 20% TIPS

- 25% diversified equities (U.S. + international)

- 10% cash equivalents

- 5% real assets exposure (optional)

Use case: Retirees with long time horizons, or those retiring in their early 60s who need purchasing power protection.

The “Bucket Strategy” allocation

The bucket approach is popular because it aligns investments to time horizons. Morningstar has long used a bucket framework for conservative retirement portfolios built around cash, bonds, and diversified equities. Morningstar

A simplified three-bucket version:

- Bucket 1 (0–2 years): cash, money markets, T-bills

- Bucket 2 (3–8 years): bonds, CDs, short-to-intermediate bond funds

- Bucket 3 (8+ years): diversified equities, inflation-sensitive growth assets

Expert insight: “Conservative is not a percentage, it is a system for funding retirement spending with fewer forced decisions.”

The Building Blocks (What to Include, What to Limit)

A conservative retirement portfolio is defined by its core ingredients. The wrong mix can create false confidence, especially when inflation and longevity are ignored.

Bonds, TIPS, and duration risk

Bonds are the backbone of conservative portfolios, but structure matters. Shorter-duration bonds reduce sensitivity to rate shifts, while longer-duration bonds can swing more than most conservative investors expect. TIPS help address inflation exposure, especially when real purchasing power is the real goal.

Practical rule: Use bonds for stability, then use TIPS to prevent inflation from silently damaging your plan.

Dividend stocks vs total-return equity

Dividend stocks can feel “safe” because they pay cash flow, but they are still equities. Dividend portfolios can underperform during certain market cycles, and they can be concentrated in sectors like financials and utilities. For most conservative retirees, a diversified equity sleeve focused on total return is often more resilient than chasing yield.

Cash, CDs, and money markets

Cash reduces volatility and supports spending needs. It also protects against forced selling. The mistake is holding so much cash that inflation becomes a guaranteed loss in real terms.

Authority snippet: “Cash is stable, but it is not always safe.”

Annuities and guaranteed income, where they fit

Annuities are not required, but they can be useful when a retiree wants to transfer longevity risk to an insurer. Schwab emphasizes aligning portfolio risk with guaranteed sources such as Social Security, pensions, and annuity income. Schwab Brokerage

For conservative planning, the right question is not “should I buy an annuity?” It is, “Do I need more guaranteed income to reduce portfolio withdrawal stress?”

How to Stress-Test a Conservative Retirement Portfolio

Most portfolios look fine in a bull market. Stress testing is how you know whether the plan is truly conservative.

A simple drawdown test

Ask: “If markets fall 20% this year, can I still fund the next 24 months of spending without selling equities?”

If the answer is no, the portfolio is not conservative enough for your cash flow needs.

Inflation scenario test

Inflation is not always high, but it is always a risk. Run your plan at 3%, 4%, and 5% inflation assumptions. If your income plan collapses under moderate inflation, you are not conservative. You are exposed.

Spending coverage and liquidity test

Map your spending into two categories:

- essential spending: housing, food, insurance, healthcare

- discretionary spending: travel, hobbies, gifts

A conservative portfolio should cover essential spending from stable sources, while discretionary spending can be funded with flexible withdrawals.

The Biggest Mistake: Being Too Conservative

The conservative label often leads retirees into a dangerous trap. They reduce volatility so aggressively that they eliminate growth. That can be riskier than holding a modest equity allocation.

How “safe” assets quietly create retirement risk

Investopedia’s recent analysis highlights a core issue: portfolios overloaded with cash and bonds can fail to keep pace with inflation and reduce long-term sustainability. Investopedia

If a retiree is withdrawing from a low-growth portfolio for 25 to 35 years, “safe” can become unsafe.

Signs your portfolio is too conservative

- You hold more than 2–3 years of spending in cash with no clear purpose

- Your long-term equity allocation is under 15% despite a long time horizon

- Your portfolio income is high, but total return is low

- Your plan ignores inflation beyond simple assumptions

- You feel safe today, but your future purchasing power is shrinking

Expert insight: “The goal is not to avoid volatility, it is to avoid selling in a downturn.”

How Entrepreneurs and High Earners Should Adapt the Conservative Model

Business owners often have a portfolio that is not reflected in their brokerage statement. Their real portfolio includes their company, their real estate, and their personal brand.

Concentration risk from business equity

If most of your net worth is tied to one operating business, your “conservative” retirement plan needs more diversification than a typical retiree’s plan. The business already acts like a high-volatility equity position. Your liquid portfolio should counterbalance it, not mirror it.

Private placements and alternatives as stabilizers (not lottery tickets)

Alternative investments can support conservative planning when used carefully, especially for accredited investors who understand liquidity and risk. Private credit, real assets, and structured income vehicles may help diversify return streams. However, they should be treated as long-term allocations with clear due diligence, not as substitutes for an emergency fund.

If you want a deeper framework on evaluating alternative strategies and risk controls, consider exploring a dedicated resource hub like /private-placements.

Tax-aware income planning, the overlooked lever

Conservative retirement strategy is not only about allocation. It is also about tax efficiency. Withdrawal sequencing, Roth conversion timing, and managing taxable income thresholds can reduce the amount you need to withdraw, which reduces portfolio strain.

This is an area where modern AI tools and planning software can help model outcomes, which connects directly to the strategy frameworks discussed in AI Strategy.

Portfolio Maintenance Rules That Work

A conservative retirement portfolio should not be managed like a day-trading account. It should be managed like a system.

Rebalancing cadence

Rebalance on a schedule, not on emotion. Many retirees use a semiannual or annual review. The goal is to avoid drift, not to chase performance.

Withdrawal sequencing and guardrails

Withdraw from stable assets when markets are down. Refill the stable bucket when markets recover. This is the practical engine behind the bucket strategy and one of the strongest defenses against sequence-of-returns risk.

When to revisit your allocation

Revisit the plan when:

- spending changes materially

- health or family obligations change

- a business sale or liquidity event occurs

- your risk tolerance changes after real market stress

Conservative Retirement Portfolio Checklist

Use this as a quick self-audit:

- I have 12–24 months of spending in stable assets

- My bond allocation matches my actual need for stability

- I understand duration and interest-rate sensitivity

- I have inflation protection (TIPS, equities, or other tools)

- My equity allocation supports my time horizon

- My withdrawal plan includes guardrails

- I rebalance with a defined schedule

- I account for taxes in withdrawal sequencing

- My plan reflects business and real estate concentration

- I can explain my portfolio strategy in one paragraph

Final Takeaway: Conservative Should Be Engineered, Not Assumed

A conservative retirement portfolio should be intentionally built around spending needs, inflation risk, and recovery capacity. It is not a single allocation that works for everyone. It is a framework that reduces forced decisions, especially during volatile markets.

Important disclosure: This article is for educational purposes only. None of the content on this article or site is financial advice. You should consult a qualified professional before making investment decisions.

Continue the conversation around business growth, strategic deal-making, and intelligent capital deployment at StephenTwomey.com.