Real Estate Professional Status, or REPS, is one of the most powerful tax strategies available to high-income investors. It allows rental real estate losses to offset active income, but only if strict IRS requirements are met. The difference between approval and denial often comes down to one factor: documentation.

What is REPS and Why Documentation Matters

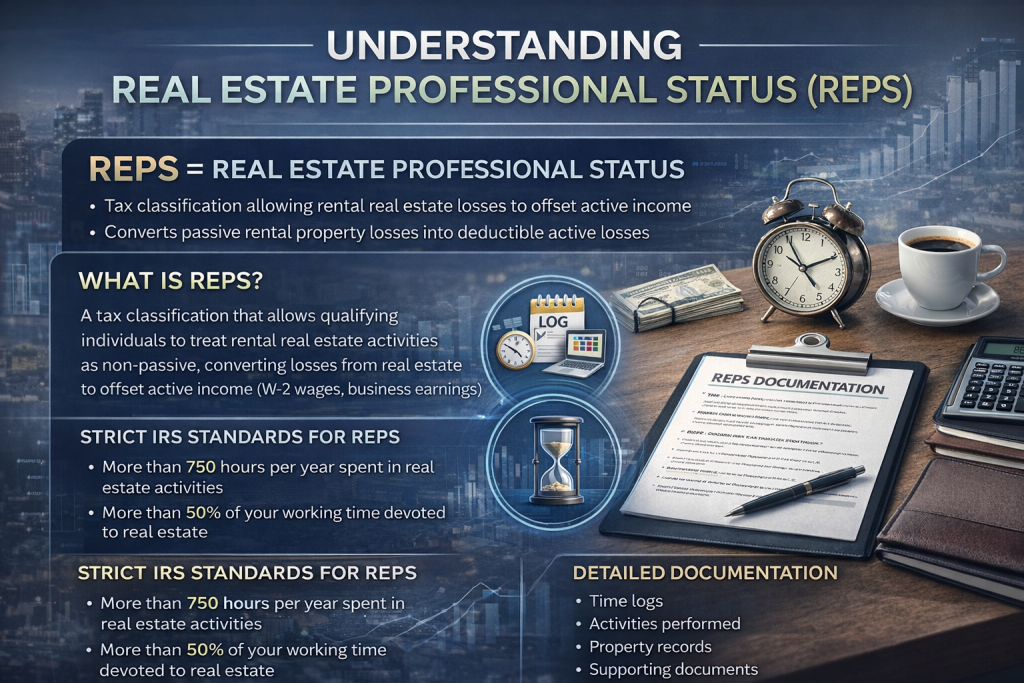

Real Estate Professional Status, or REPS, is a tax classification that allows qualifying individuals to treat rental real estate activities as non-passive. This creates a significant advantage. It allows losses from real estate to offset active income such as W-2 wages or business earnings.

However, REPS is not automatic. It is a position that must be proven, not assumed. The IRS applies strict standards, and documentation is the deciding factor in whether the benefit is allowed or denied.

Overview of Real Estate Professional Status

To qualify for REPS, a taxpayer must meet two core tests each year:

- Spend more than 750 hours in real estate activities

- Spend more than 50 percent of total working time in those activities

In addition, the taxpayer must materially participate in their real estate operations. This means they are actively involved in managing, operating, or making decisions about their properties.

Qualifying activities may include:

- Property management and leasing

- Overseeing renovations

- Reviewing financial performance

- Communicating with tenants or contractors

Passive ownership alone does not qualify. The IRS expects clear, consistent involvement.

IRS Audit Risk and Documentation Requirements

REPS is one of the most commonly audited positions in real estate investing. The reason is simple. The tax benefits can be substantial, and the rules are often misunderstood or loosely applied.

During an audit, the IRS focuses on two areas:

- Total hours worked

- Evidence of material participation

This is where documentation becomes critical. The IRS does not rely on estimates or general statements. It requires detailed, time-based records supported by real activity.

Strong documentation includes:

- Contemporaneous time logs

- Emails and communication records

- Calendars and task tracking

- Supporting documents tied to each activity

Weak documentation often leads to disallowed losses, even if the taxpayer actually qualified.

A simple principle applies. If you cannot prove it, the IRS assumes it did not happen.

Core Documentation Best Practices REPS Accredited Investors Must Follow

For accredited investors pursuing Real Estate Professional Status, documentation is the backbone of the strategy. The tax benefit can be substantial, but the IRS does not reward broad claims or informal estimates. It expects a clear record showing that real estate activity was regular, substantial, and directly tied to the taxpayer’s role.

The strongest approach is to treat REPS like a business function. That means tracking time consistently, preserving evidence across properties, and maintaining records as work happens, not months later during tax filing. Investors who own multiple assets, participate in syndications, or manage renovations should assume that every hour claimed may need support. A defensible REPS position usually combines time logs, emails, calendars, lease activity, invoices, meeting notes, and property management records. Good documentation does more than satisfy compliance. It protects the credibility of the entire tax position. For investors with meaningful passive losses, disciplined recordkeeping can be the difference between preserving deductions and losing them in an audit.

Time Tracking and Hour Logs

Time tracking is one of the most important pillars of REPS compliance. To qualify, a taxpayer generally needs to prove at least 750 hours of qualifying real estate activity and that more than half of total working time was spent in real estate trades or businesses. That standard is difficult to defend without detailed hour logs created throughout the year.

The best logs are specific and consistent. Each entry should include the date, amount of time spent, property or activity involved, and a short but clear description of the work performed. Entries such as reviewing leases, coordinating contractors, analyzing operating reports, handling tenant issues, or overseeing capital improvements are far stronger than vague phrases like “real estate work.” Digital tools such as calendar apps, spreadsheets, or time-tracking software can help create a reliable system. The key is accuracy, not inflation. Overstated or reconstructed hours can quickly undermine a claim. For accredited investors with multiple holdings, disciplined time tracking shows that real participation was both ongoing and operationally meaningful.

Material Participation Evidence

Hour counts alone are not enough. REPS claims are much stronger when they are backed by evidence of material participation. In practice, that means showing that the investor was actively involved in managing, operating, or making decisions related to the real estate activity. The IRS wants proof that participation was real, not passive or purely financial.

Strong supporting evidence can include email threads with brokers, tenants, contractors, attorneys, and property managers. It can also include meeting notes, lease negotiations, renovation approvals, budgets, invoices, travel records, call logs, and property management reports. These materials help connect the hours claimed to actual business activity. For accredited investors, this is especially important when holdings are spread across entities or properties, because passive ownership alone does not establish participation. Documentation should show judgment, oversight, and direct involvement in decisions that affect the asset. A well-supported file creates a more complete story. It tells the IRS not only how much time was spent, but also why that time reflects meaningful operational participation.

Contemporaneous Recordkeeping Standards

Contemporaneous recordkeeping means creating and preserving records close to the time the work actually happens. This standard matters because the IRS and tax courts often view reconstructed logs with skepticism, especially when they appear polished but unsupported. A taxpayer may genuinely remember being active during the year, but memory is not a substitute for evidence.

For REPS purposes, contemporaneous records do not need to be overly complex. What matters is consistency and timing. A calendar entry, saved email, project update, property note, or weekly time log can all support the record when maintained as part of a normal workflow. The strongest documentation systems are built into the investor’s routine, not assembled at year-end by a CPA. Accredited investors should think in terms of audit readiness from the start. Save records in organized folders by property, month, and activity type. Maintain summaries, but also keep the underlying support. When documentation is created in real time, it is far easier to defend and far more credible under scrutiny.

What the IRS Looks for in a REPS Audit

Common Red Flags

Auditors often flag:

- Round number hour entries

- Missing dates or inconsistent logs

- Excessive hours relative to full-time employment

Acceptable vs Weak Documentation

Strong documentation includes:

- Digital logs with timestamps

- Supporting emails and receipts

- Calendar integrations

Weak documentation includes:

- Reconstructed spreadsheets

- Generic summaries

- Unsupported estimates

“The IRS does not audit your intent. It audits your records.”

Case Law Insights

Cases like Moss v. Commissioner and Bailey v. Commissioner highlight a consistent theme. Taxpayers lose when documentation is vague or reconstructed. They win when records are detailed and credible.

Tools and Systems for REPS Documentation

Digital Time Tracking Tools

Platforms like Toggl, Harvest, and Clockify allow investors to track hours with precision. These tools create defensible logs that align with IRS expectations.

CRM and Property Management Systems

Systems like AppFolio or Buildium provide operational records. They track tenant communications, maintenance requests, and lease activity.

These systems create a secondary layer of documentation that supports time logs.

Structuring a Documentation Workflow

A structured workflow includes:

- Daily time tracking

- Weekly review of entries

- Monthly export and backup

Storing records in cloud systems ensures accessibility during audits.

Advanced Strategies to Strengthen REPS Compliance

Grouping Elections and Documentation

Grouping multiple properties into a single activity can simplify compliance. However, documentation must reflect this election and demonstrate participation across the grouped portfolio.

Combining REPS with Short-Term Rentals

Short-term rentals may qualify as non-passive without REPS if material participation is met. When combined strategically, documentation becomes even more critical.

Working with CPAs and Tax Advisors

Experienced real estate CPAs understand audit expectations. They help structure documentation systems and review logs before filing.

For deeper tax strategies, see /real-estate-tax-strategies.

REPS Documentation Checklist for Investors

Daily, Weekly, and Annual Tracking

Daily:

- Log hours and tasks

Weekly:

- Review and categorize activities

Annually:

- Compile summaries and supporting documents

Audit-Ready File Structure

Organize records into:

- Time logs

- Emails and communications

- Financial records

- Property activity reports

This structure ensures quick access during audits.

Common Mistakes Investors Make

Reconstructed Logs

Creating logs at year-end is one of the most common errors. Courts consistently reject these records.

Overstating Hours

Inflated hours damage credibility. Logs must align with realistic schedules.

Lack of Supporting Evidence

Time logs alone are not enough. Supporting documentation is essential to validate entries.

“If your documentation is weak, your tax position is weak.”

Final Thoughts on REPS Documentation Strategy

REPS offers significant tax advantages, but it demands discipline. Investors who treat documentation as a core business process, not an afterthought, are far more likely to succeed.

The most effective approach combines real-time tracking, supporting evidence, and professional oversight. This transforms REPS from a risky claim into a defensible strategy.

Explore more insights on scaling businesses, building strategic partnerships, and navigating modern investment ecosystems at StephenTwomey.com.

Disclosure: None of the content in this article or on this site should be considered financial or tax advice. Consult a qualified professional before making any investment or tax decisions.