Investing In A Private Placement 506(B), What To Expact

For most people, the interesting part of a 506(b) private placement is not the legal label. It is the lived experience behind it. What does the process actually feel like once the term sheet language and securities-law references are stripped away? How does access happen, what kind of paperwork shows up, who is actually running the deal, and what does life as a limited partner look like after the money is wired?

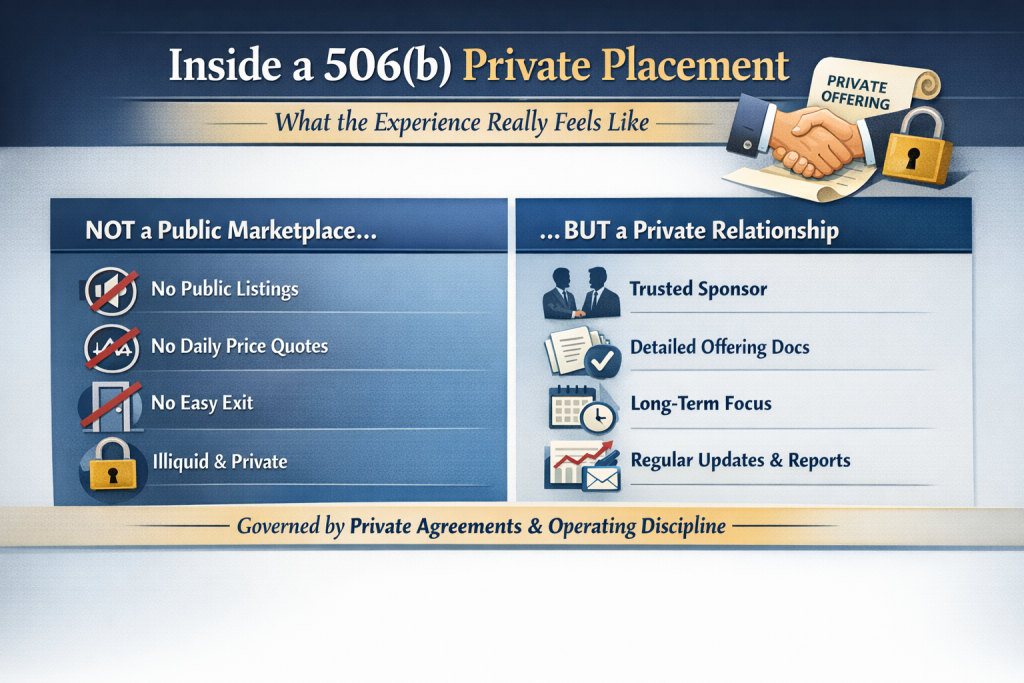

Rule 506(b) sits within Regulation D and serves as a private-placement safe harbor under federal securities law. In practical terms, it gives issuers a way to raise an unlimited amount of capital without registering the offering publicly, so long as they stay within the rule’s boundaries. One of the most important of those boundaries is that 506(b) offerings cannot be made through general solicitation or public advertising. The structure is intentionally private, which is one reason the investor experience tends to feel more relationship-driven and less transactional than buying something in a brokerage account.

That difference matters. A 506(b) investment usually does not begin with a public pitch deck on social media or a mass-marketed campaign. It more often begins with an existing relationship, a private introduction, a longstanding network connection, or a sponsor the investor already knows. The atmosphere is different from the start. It is quieter, more document-heavy, and more dependent on trust, diligence, and communication. None of that automatically makes it better or worse than a public-market investment. It simply makes it a different kind of experience.

It also needs to be said clearly at the outset that this article is educational only. It is not investment, legal, or tax advice, and it is not an offer to sell or a solicitation of an offer to buy any security. That distinction is especially important in a topic like this, because Rule 506(b) exists inside a very specific regulatory framework.

What Is A 506(B) Private Placement?

A 506(b) private placement is a securities offering conducted under Regulation D. In practical terms, it gives companies objective standards they can rely on when raising capital privately. Under the rule, an issuer can raise an unlimited amount of money and sell securities to an unlimited number of accredited investors. The rule also allows up to 35 non-accredited investors, provided they meet a sophistication standard and the required disclosures are handled properly.

That legal structure shapes the experience for everyone involved. Public investments are designed for broad availability and continuous market visibility. A 506(b) investment is different. There is typically no public market for the interest, no constant price quote, and no easy ability to exit on demand. The value of the experience tends to depend less on daily visibility and more on the quality of the sponsor, the clarity of the documents, the discipline of the reporting process, and the investor’s willingness to think on a longer time horizon.

In other words, the investor is not stepping into a liquid public marketplace. The investor is stepping into a private relationship governed by offering documents, economic rights, and whatever operating discipline the sponsor and general partner bring to the table. That is a much better way to understand what it feels like in practice.

Requirements To Invest In A 506(B)

One of the first practical questions any reader has is whether they would even qualify to participate. On that point, the answer is more nuanced than many summaries make it sound.

A 506(b) offering does not require every investor to be accredited. Companies can sell to an unlimited number of accredited investors and up to 35 non-accredited investors. But that does not mean every offering is open to a broad mix of participants. In practice, many sponsors limit participation to accredited investors anyway, partly because involving non-accredited investors can increase disclosure obligations and complexity. So while the rule itself allows a broader range than people sometimes assume, many actual deals still function as accredited-investor-heavy offerings.

The accredited investor definition comes from Rule 501 of Regulation D. For individuals, the two most familiar routes are income and net worth. A person generally qualifies if they have earned more than $200,000 individually in each of the two most recent years, or $300,000 jointly with a spouse or spousal equivalent, with a reasonable expectation of reaching the same level in the current year. A person may also qualify by having net worth above $1 million, individually or jointly with a spouse or spousal equivalent, excluding the value of the primary residence. There are also additional categories tied to professional certifications and certain entity structures.

For someone who is not accredited, participation is still possible in some 506(b) offerings, but only under stricter conditions. The key concept is sophistication. The non-accredited investor must have enough financial and business knowledge to evaluate the merits and risks of the investment, either personally or with help from a purchaser representative. That standard matters because private placements do not come with the same public-market protections and disclosures people may be used to seeing elsewhere.

The practical side of qualification tends to feel less glamorous than the idea of access to a private deal. It usually involves paperwork. An investor questionnaire is common. A subscription agreement is standard. There may be a private placement memorandum, an operating agreement or limited partnership agreement, entity documents if the investor is coming in through an LLC or trust, and a set of representations about eligibility, risk tolerance, and acknowledgment of the offering terms. In a 506(b) deal, the issuer generally needs a reasonable basis for believing the investor is eligible under the terms of the offering, even though 506(c) has the more formal verification requirement.

That is one of the first places where a private placement starts to feel real. It stops being an abstract alternative investment category and starts becoming a structured legal and financial relationship.

Sponsor, General Partner, And Limited Partner

A lot of confusion in private placements comes from the vocabulary. Sponsor, GP, and LP are often used casually, and sometimes interchangeably, even though they are not the same thing.

The sponsor is usually the firm or operating team that originates and organizes the opportunity. In real estate and many private-market structures, the sponsor is the group sourcing the deal, assembling the thesis, structuring the raise, coordinating the offering documents, and driving the investment narrative. It is often the name the investor knows first.

The general partner, or GP, is usually the control entity. The GP manages the investment, makes decisions, oversees execution, and carries responsibility for operations and reporting within the structure. In some deals the sponsor and the GP are closely linked, and in others the sponsor is the outward-facing brand while the GP is the legal manager behind it. The exact structure can vary, but the GP is generally the party with control.

The limited partner, or LP, is the investor on the passive side of the arrangement. The LP contributes capital and participates economically under the terms laid out in the governing documents, but usually does not run the investment day to day. That does not make the LP irrelevant. It simply means the LP’s role is economic rather than managerial.

For many investors, this relationship ends up defining the feel of the investment opportunity more than any marketing summary ever could. Being an LP often means there is a front-loaded period of diligence and decision-making, followed by a long stretch in which the investor is relying on the GP and sponsor for execution, reporting, and judgment. That dynamic can feel smooth and professional in a well-run deal, or frustrating and opaque in a poorly run one. The structure itself does not guarantee the experience. The people inside it shape the experience.

What The Process Usually Feels Like

A 506(b) investment often begins quietly. Because general solicitation is prohibited, the path into the opportunity usually runs through a pre-existing relationship or a private introduction rather than broad public promotion. That alone gives the process a different tone. It tends to feel more selective, but also more dependent on context and familiarity.

From there, the diligence phase begins. This is the part where the investor is usually reviewing the private placement memorandum if one is provided, reading the subscription materials, studying the economics, trying to understand the fee structure, evaluating the business plan, and deciding whether the sponsor’s communication style inspires confidence. Some deals feel crisp at this stage. Others feel rushed or vague. Investors notice that difference quickly. In a private placement, the quality of the materials is not just cosmetic. It often serves as an early indicator of how disciplined the operation may be after closing.

Once the decision is made to move forward, the process becomes administrative. The investor fills out the questionnaire, signs the subscription documents, submits any required supporting information, and wires funds according to the instructions provided. At that point, the experience shifts. Before funding, the investor is evaluating. After funding, the investor is monitoring.

That transition is one of the defining emotional features of being an LP. There is often a brief period of intense scrutiny up front, followed by a much longer period in which the quality of the experience depends on visibility, reporting, responsiveness, and whether the sponsor does what it said it would do. A private placement is not a constant stream of price discovery. It is more often a long-term process of observing execution through periodic updates and formal notices.

Reporting Platforms And The Investor Dashboard Experience

This is one of the least discussed but most tangible parts of private investing. A lot of what it feels like to be an LP comes down to infrastructure.

In a modern private-placement environment, the investor portal often becomes the central interface between the LP and the investment. Juniper Square is one of the clearest examples. Platforms like this connect LPs and GPs across workflows including fundraising, investor onboarding, compliance, treasury, reporting, and investor communications.

That matters because a well-run portal changes the experience in practical ways. Instead of chasing email attachments, asking for old documents, or manually tracking capital activity, an LP may have one place to review subscription records, archived updates, notices, transaction history, account statements, tax documents, and distribution information. The portal does not replace sponsor quality, but it can make the investment feel more orderly, more transparent, and easier to manage over time.

The reverse is also true. Weak reporting infrastructure can make even a promising investment feel harder to live with. If documents are scattered, notices are delayed, and reporting lacks consistency, the friction adds up. That is one reason experienced investors often care about operational systems more than outsiders expect. In private markets, administrative professionalism is not a side issue. It is part of the product.

What Good Communication Usually Looks Like

Communication carries unusual weight in a 506(b) investment because the structure is private and typically illiquid. An LP usually does not have the comfort of public-market transparency, daily price visibility, or easy exits. That means the sponsor’s communication habits can become a major part of how the investment is experienced.

Good communication is rarely about volume alone. It is more about clarity, consistency, and tone. Investors generally notice whether updates arrive on a predictable cadence, whether capital activity is explained cleanly, whether bad news is handled directly instead of buried, and whether documents are easy to access when needed. A sponsor does not need to narrate every detail of operations, but it helps when the communication creates a sense that the investment is being handled by adults who understand that investor confidence is built through discipline, not marketing flourish.

This is one of the most understated truths in private placements. Returns matter, of course. But so does the feeling that the sponsor respects the investor’s capital enough to communicate with precision and candor. In a long-duration, illiquid structure, that can shape the investor experience almost as much as the economics themselves.

Returns, Risk, And Liquidity

Any honest article on private placements has to resist the temptation to flatten outcomes into a single story. There is no universal 506(b) experience when it comes to performance. Results vary based on the asset class, the capital structure, the quality of the sponsor, the use of leverage, the fee design, the market cycle, and the execution on the ground.

Some investors are drawn to private placements because they believe certain opportunities may behave differently from the public markets. That can be a reasonable observation in some contexts, and it is part of why terms like uncorrelated exposure or uncorrelated alpha show up in conversations around alternatives. But the idea needs to be handled with care. Lower correlation does not automatically mean lower risk, better returns, or smoother outcomes. It simply points to the possibility that the return drivers may be different from those in public equities or bonds.

Liquidity is often the bigger reality check. Private placements can tie up capital for years. That is not a footnote. It is one of the central features of the experience. For the right investor, that may be acceptable. For the wrong investor, it can become the defining frustration of the entire investment. A person who is comfortable with a long hold and limited interim liquidity tends to experience the structure very differently from someone who expects optionality on short notice.

Risk disclosures also deserve more respect than they usually get. In a private offering, those disclosures are not ornamental. They are there because real uncertainty exists. The investor is often relying on a closed set of documents, a specific management team, and a sponsor’s ability to execute a plan that may unfold over years. That can work well. It can also disappoint. The point is not to be cynical about the structure. It is to take the structure seriously.

506(B) Vs 506(C)

The distinction between 506(b) and 506(c) is easy to summarize, but it has meaningful consequences for how the investment process feels.

Under 506(b), general solicitation is prohibited. Under 506(c), it is permitted. That means 506(c) offerings can be publicly marketed, while 506(b) offerings are expected to remain within a more private, relationship-based framework. The sourcing process is different from the outset. A 506(b) opportunity often reaches an investor through familiarity. A 506(c) opportunity can reach an investor through broad visibility.

The investor-qualification rules also differ. A 506(c) offering requires all purchasers to be accredited investors, and the issuer must take reasonable steps to verify that status. By contrast, 506(b) permits sales to unlimited accredited investors and up to 35 non-accredited but sophisticated investors, with the issuer operating under a reasonable-belief standard rather than the same formal verification framework.

That difference can affect tone, onboarding, and expectations. Even when the underlying investment is similar, a 506(b) offering may feel more private and relationship-centered, while a 506(c) offering may feel more standardized or publicly accessible. Neither format automatically says anything about quality. It simply changes the path by which the investor gets there.

My Personal Experience Investing In A 506(B) Since 2022

Legal Disclaimer: The following reflects one investor’s personal experience and is provided for general informational purposes only. It is not financial, legal, or tax advice, and it is not an offer to sell or a solicitation of an offer to buy any security. Private placements involve risk, including the possible loss of principal. Any investment decision should be made only after reviewing the relevant offering documents and consulting qualified advisors.

I have been a limited partner in a Rule 506(b) private placement investment since 2022. I cannot speak for every private placement opportunity, and I do not suggest that every offering operates the same way or produces similar results. The one I have been part of has been strong from both an operational and investor-experience standpoint. Communication has been clear, the dashboard has been easy to use, and the reporting through Juniper Square has made it simple to stay organized and informed over time.

From my perspective as an LP, one of the most important parts of the experience has been understanding the structure of the relationship. The GP is the party managing the investment, making decisions, and handling execution. The LP is participating as a passive investor under the rights and economics set out in the offering documents. In many private placements, the sponsor is the team or firm organizing the opportunity, while the GP is the legal manager overseeing it. In the investment I have been part of, that structure has translated into strong communication, a straightforward reporting process, and useful access to a network of other investors.

The returns in my particular investment have also been strong, and from my own vantage point they have behaved differently from traditional public-market exposure. That said, I would not generalize that outcome to every private placement. Private investments vary widely, and no individual experience should be read as representative of the category as a whole.

Final Thoughts On What It Is Like Investing In A Private Placement 506(B)

Investing in a 506(b) private placement usually feels less like buying a product and more like entering a structure. The experience is shaped by eligibility rules, documents, people, reporting discipline, and time horizon. For an LP, there is often an early burst of diligence followed by a much longer period of observing how the sponsor and GP operate under real conditions.

That is why the best way to understand a 506(b) investment is not to stop at the legal definition. The legal definition matters, and regulatory guidance is the right place to start. But the actual experience turns on quieter things: whether the relationship was built properly, whether the documents are clear, whether the reporting is organized, whether the communication is candid, and whether the investor entered the structure with realistic expectations about risk and liquidity. Rule 506(b) provides the framework. The human and operational side determines what it is actually like to live inside one.