Retirement portfolio allocation defines how capital is positioned to support income, preserve purchasing power, and manage risk over decades. For sophisticated and accredited investors, allocation decisions often matter more than individual security selection. A modern approach requires moving beyond outdated models and understanding how assets behave in changing market environments.

What is Retirement Portfolio Allocation

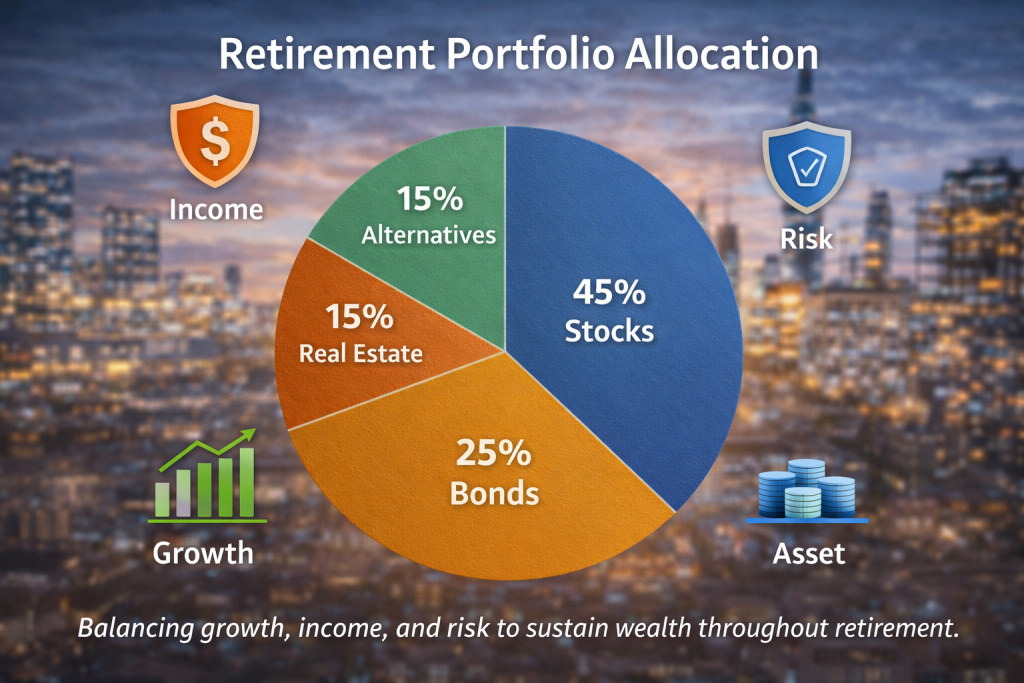

Retirement portfolio allocation is the process of distributing capital across asset classes to balance growth, income, and risk. The objective is not maximum return, but durability of wealth throughout retirement.

Why allocation matters more than individual investments

Individual investments come and go. Allocation decisions shape long-term outcomes. Studies consistently show that asset allocation explains the majority of portfolio return variability over time, not stock picking or market timing.

Allocation vs diversification explained clearly

Diversification spreads risk across holdings. Allocation determines how much risk exists in the first place. A diversified portfolio can still fail if the underlying allocation is misaligned with retirement income needs.

Core Asset Classes in a Retirement Portfolio

A well-constructed retirement portfolio allocation begins with a clear understanding of core asset classes and the role each plays over time. Retirement is not a single financial phase. It is a multi-decade period that requires growth, income stability, and flexibility under changing market conditions. The purpose of allocation is not to chase returns, but to coordinate assets so they work together under stress. Equities, fixed income, and cash each serve a specific function within this structure. When balanced correctly, they help manage volatility, protect purchasing power, and support predictable withdrawals. When misaligned, even strong market performance can fail to translate into retirement security. For long-term success, these asset classes must be evaluated not in isolation, but in how they interact across economic cycles, interest rate environments, and personal income needs.

Equities and Long-Term Growth

Equities are the primary engine of long-term growth in a retirement portfolio. Their role is to outpace inflation and preserve purchasing power over extended time horizons. Even in retirement, portfolios that eliminate equities entirely often face longevity risk, especially as life expectancy increases. Stocks provide exposure to corporate earnings, innovation, and economic expansion, all of which contribute to real return potential. However, equity allocation in retirement must be calibrated carefully. Excessive exposure can amplify volatility and increase the risk of selling during market downturns. Insufficient exposure, on the other hand, can erode future income capacity as inflation compounds. The focus shifts from aggressive appreciation to sustainable growth. Dividend-paying equities, value-oriented strategies, and diversified global exposure are often favored over concentrated bets. In this context, equities are less about speculation and more about maintaining long-term balance within the broader retirement portfolio allocation.

Fixed Income and Capital Preservation

Fixed income plays a stabilizing role in retirement portfolio allocation by providing income and reducing overall volatility. Bonds, notes, and other income-producing instruments help offset equity fluctuations and create predictable cash flows. In retirement, this predictability becomes increasingly valuable as withdrawals begin. However, fixed income is not without risk. Rising interest rates can reduce bond prices, while inflation can erode real returns. As a result, retirees must pay close attention to duration, credit quality, and structure. Shorter-duration bonds may reduce interest rate sensitivity, while diversified credit exposure can enhance yield without excessive risk. Fixed income should be viewed as a risk management tool rather than a return driver. Its primary purpose is capital preservation, income support, and behavioral stability. When designed properly, fixed income allows other parts of the portfolio to remain invested during market stress, which supports long-term sustainability.

Cash and Liquidity Management

Cash is often underestimated, yet it plays a critical role in retirement portfolio allocation. Liquidity provides flexibility, psychological comfort, and protection against forced asset sales during market downturns. Cash reserves are typically used to fund near-term living expenses, unexpected costs, and short-term obligations. This buffer allows long-term assets to remain invested through periods of volatility. However, excessive cash allocation introduces its own risk. Inflation steadily erodes purchasing power, turning idle cash into a long-term liability. The key is balance. Cash should be sufficient to cover planned withdrawals and contingencies, but not so large that it materially drags portfolio performance. Many retirement strategies aim to maintain one to three years of spending needs in cash or cash equivalents. Within a broader allocation framework, cash is not an investment return tool. It is a control mechanism that supports disciplined decision-making and long-term portfolio resilience.

Rethinking Traditional Allocation Models

Many retirement strategies still rely on frameworks developed in very different economic conditions. These models deserve closer scrutiny.

Limitations of the 60/40 portfolio

The 60 percent equity, 40 percent bond model assumes negative correlation between stocks and bonds. In inflationary environments, that relationship often breaks down, increasing portfolio drawdowns when protection is needed most.

Inflation and correlation risk

Inflation impacts both purchasing power and asset correlations. When inflation rises, traditional assets can decline together. Allocation strategies that ignore this risk often underestimate real-world volatility.

“Inflation exposes the assumptions hidden inside traditional portfolio models.”

The Role of Alternative Investments in Retirement

For accredited investors, alternative investments can address gaps left by public markets. These assets are not replacements, but complements when used correctly.

Private equity and private credit

Private equity targets long-term growth through operational value creation rather than market multiples. Private credit emphasizes income and downside protection, often with floating-rate structures that respond to interest rate changes.

Real assets and inflation hedging

Real estate, infrastructure, and other real assets offer income streams tied to tangible value. These assets often perform better during inflationary periods than nominal financial instruments.

Risk considerations for accredited investors

Alternatives involve illiquidity, manager selection risk, and longer holding periods. Proper sizing and due diligence are essential. Allocation discipline matters more than enthusiasm.

“Alternatives introduce complexity, but they also introduce flexibility that public markets cannot offer.”

Portfolio Allocation by Life Stage

Retirement allocation is not static. It evolves as time horizon, income needs, and risk capacity change.

Pre-retirement accumulation phase

During accumulation, growth remains the priority. Allocation decisions should focus on building a resilient base while gradually preparing for future income needs.

Early retirement and drawdown planning

The first years of retirement carry the highest sequence-of-returns risk. Allocation must support withdrawals while limiting exposure to large early losses.

Late retirement and capital efficiency

Later stages emphasize income reliability and estate considerations. Capital efficiency becomes more important than headline returns.

Risk Management and Behavioral Discipline

Technical allocation decisions fail without behavioral discipline. Risk management is as much psychological as mathematical.

Sequence-of-returns risk

Poor returns early in retirement can permanently impair portfolios. Managing this risk requires liquidity planning, flexible withdrawals, and diversified income sources.

Rebalancing and downside control

Rebalancing enforces discipline by trimming excess risk and reinvesting into undervalued assets. It also prevents portfolios from drifting away from their intended risk profile.

Building a Modern Retirement Allocation Framework

A modern framework integrates traditional and alternative assets with clear objectives. It focuses on resilience rather than prediction.

Aligning allocation with income needs

Income requirements should drive allocation decisions. Growth assets support long-term sustainability, while income assets support lifestyle stability.

Stress testing and scenario analysis

Stress testing portfolios against inflation spikes, rate shocks, and prolonged downturns reveals vulnerabilities that static models overlook. Institutional investors rely on this process for a reason.

For a deeper look at advanced portfolio construction, explore our perspective on alternative investments at /alternative-investments.

Key Takeaways for Accredited and Sophisticated Investors

Retirement portfolio allocation is no longer about simple stock and bond percentages. It is about managing multiple risks over an extended timeline. Investors who adapt their allocation frameworks gain flexibility, resilience, and control.

“The most effective retirement portfolios are designed for endurance, not optimism.”

Important Disclosure

This content is for educational purposes only. It does not constitute financial, investment, tax, or legal advice. Readers should consult qualified professionals before making financial decisions.

For perspectives at the intersection of entrepreneurship, capital allocation, and long-term business value creation, visit StephenTwomey.com.