Financial advisor fees are a meaningful expense for investors, especially those with complex portfolios. Many still ask whether these fees reduce taxable income. The answer has changed significantly, and understanding the current rules is essential for effective wealth planning.

Are Financial Advisor Fees Tax Deductible in 2025

For most individual investors, financial advisor fees are not tax deductible on personal tax returns as of 2025. This change stems from federal tax reform that eliminated several itemized deductions.

While this surprises many investors, the rule is clear for standard investment advisory fees tied to personal accounts. There are exceptions, but they depend on how income is earned and how fees are structured.

How Financial Advisor Fees Were Treated Before the Tax Cuts and Jobs Act

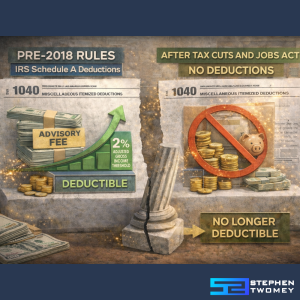

Before 2018, advisory fees received more favorable treatment under IRS rules. Investors who itemized deductions could often deduct a portion of these costs.

Miscellaneous Itemized Deductions Explained

Investment advisory fees were classified as miscellaneous itemized deductions. These included expenses related to tax preparation and portfolio management.

The 2 Percent AGI Threshold

Only expenses exceeding 2 percent of adjusted gross income qualified. For high earners, this often limited the actual benefit, even before the deduction was removed.

What Changed Under the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act of 2017 reshaped deduction rules across the board.

Suspension of Advisory Fee Deductions

The law suspended all miscellaneous itemized deductions subject to the 2 percent AGI threshold. Investment advisory fees fell squarely into this category.

Timeline and Current Status

This suspension applies through at least 2025. Unless Congress acts, these deductions remain unavailable for individual taxpayers.

Which Financial Advisory Fees May Still Be Deductible

Although most personal financial advisor fees are no longer deductible under current U.S. tax law, there are still specific situations where advisory costs may qualify for favorable tax treatment. The key factor is not the service itself, but the context in which the fee is incurred. Fees connected to producing taxable income, managing entities, or administering fiduciary responsibilities can fall under different IRS rules than personal investment advice.

For business owners, real estate investors, and individuals involved in trusts or retirement planning, this distinction matters. Understanding where deductions may still apply requires careful classification of expenses, proper documentation, and alignment with IRS definitions of ordinary and necessary costs. Below are the primary categories where financial advisory fees may still be deductible, provided they meet specific criteria and are structured correctly.

Fees Related to Business or Rental Income

Financial advisory fees may be deductible when they are directly related to operating a business or managing income producing rental property. If an advisor provides services tied to cash flow planning, capital allocation, debt strategy, or financial management for a business entity, those fees can often be treated as ordinary and necessary business expenses. The same applies to rental real estate activities where advisory services support acquisition decisions, financing analysis, or long term income planning. The IRS generally allows deductions when the expense has a clear and direct connection to generating taxable income.

However, the burden of proof rests with the taxpayer. Fees must be properly invoiced, clearly described, and separated from personal financial planning services. Mixing personal and business advice into a single fee can jeopardize deductibility. Business owners and real estate investors should work closely with their CPA to ensure advisory expenses are categorized accurately and reported correctly on the appropriate tax forms.

Trust and Estate Advisory Fees

Trust and estate advisory fees remain one of the more nuanced areas where deductions may still apply. The IRS allows deductions for expenses that are unique to the administration of a trust or estate and would not have been incurred if the property were held individually. This can include fees for investment management, fiduciary oversight, tax compliance, and distribution planning when those services are necessary to fulfill fiduciary duties.

The distinction is critical. If an advisory service is considered personal investment advice, it may not be deductible. If it is required to administer the trust or estate under governing documents or state law, it may qualify. Following changes introduced after the Tax Cuts and Jobs Act, courts and IRS guidance have clarified that only expenses specific to fiduciary responsibilities are eligible. Trustees and beneficiaries should ensure advisory fees are properly allocated and supported by detailed records to withstand scrutiny.

Retirement Account Related Fees

Retirement account related advisory fees are not deductible as personal itemized deductions, but they can still impact taxes indirectly depending on how they are paid. When advisory fees are paid directly from certain retirement accounts, such as traditional IRAs, the account balance is reduced without creating a taxable event. This can lower future required minimum distributions and reduce taxable income over time. While this does not constitute a deduction, it can improve after tax outcomes for retirees.

In contrast, paying retirement advisory fees out of pocket with after tax dollars provides no tax benefit under current law. The strategy around how and where fees are paid becomes especially important for high net worth individuals managing large retirement balances. Coordination between the advisor and tax professional is essential to ensure compliance with account rules while optimizing long term tax efficiency.

Implications for Accredited Investors and High Net Worth Individuals

For accredited investors, the issue is less about deductibility and more about structuring.

Private Placements and Alternative Investments

Advisory fees connected to private equity, hedge funds, or private placements may be embedded at the entity level. This can shift tax treatment depending on the investment structure. More detail on this can be found in discussions on alternative investment strategy at /alternative-investments.

Structuring Fees for Tax Efficiency

Entity choice, allocation methods, and fee categorization all influence outcomes. Coordination between advisors and CPAs is essential.

Common Misconceptions About Advisor Fee Deductions

Many investors still misunderstand how financial advisor fees are treated under current tax law. Much of the confusion comes from outdated rules, oversimplified online advice, or assumptions based on income level. Clarifying these misconceptions is essential for setting realistic expectations and making informed planning decisions.

Financial advisor fees are always tax deductible

A common belief is that advisor fees automatically reduce taxable income. This was partially true before 2018, but it no longer applies to most individuals. Under current law, standard investment advisory and portfolio management fees paid from personal accounts are not deductible. The IRS classification of these expenses, not their purpose, determines deductibility.

High income or accredited status restores deductibility

Some investors assume that earning more or qualifying as an accredited investor changes the tax treatment of advisor fees. Income level does not affect whether a deduction is allowed. The tax code applies the same rules regardless of net worth. What matters is how the fee is categorized and whether it is tied to business, rental, or fiduciary income.

Renaming fees changes their tax treatment

Another misunderstanding is that re-labeling advisory fees as consulting or planning fees makes them deductible. The IRS looks at substance over labels. If the service relates to personal investment management, the fee is treated the same regardless of how it appears on an invoice. Documentation and economic reality carry more weight than terminology.

Fees paid from retirement accounts are tax deductions

Fees paid directly from retirement accounts are often mistaken for deductible expenses. In reality, they are not claimed as deductions on a tax return. Instead, these fees reduce the account balance, which may lower future taxable distributions. This is a cash flow and efficiency consideration, not a deduction.

All advisory fees are permanently non deductible

While most personal advisory fees are not deductible, some investors assume no exceptions exist. This is incorrect. Fees tied directly to operating a business, managing rental property, or administering certain trusts may still qualify as deductible expenses. These situations require careful structuring and coordination with a qualified tax professional to remain compliant.

Strategic Tax Planning Considerations Going Forward

The loss of deductibility does not mean fees should be ignored. It means they must be evaluated as part of a broader wealth strategy.

Investors should focus on net after-tax returns, not isolated deductions. In complex portfolios, especially those involving private capital, tax efficiency is driven by structure and long-term planning, not line-item write-offs.

According to IRS guidance outlined in Publication 529, understanding expense classification is essential for compliance and planning.

Continue the conversation around business growth, strategic deal-making, and intelligent capital deployment at StephenTwomey.com.

Disclosure: This article is for informational purposes only. Nothing on this site constitutes financial, tax, or legal advice. Consult a licensed professional before making financial decisions.