Disclosure: None of the writing on this article or site is financial advice.

This guide explains how allocation strategies can change as investors age. It helps professionals, entrepreneurs, and accredited investors think about allocation in a structured way.

What is Age-Based Portfolio Allocation?

Age-based portfolio allocation is a framework for structuring an investment portfolio according to an investor’s stage of life. The core idea is that the mix of assets should evolve as financial goals, income stability, and time horizon change. Early in a career, portfolios often emphasize growth-oriented assets such as equities because investors have more time to recover from market volatility. As individuals move closer to retirement, allocations typically shift toward assets that prioritize capital preservation, income generation, and reduced volatility. Age functions as a proxy for these evolving priorities, making it a practical starting point for portfolio construction rather than a rigid rule.

This approach is widely used because it provides structure without requiring constant decision-making. Target-date funds, model portfolios, and institutional retirement plans are all built on age-based allocation principles. However, age-based allocation is not meant to operate in isolation. It works best when combined with personal factors such as savings rate, income predictability, liquidity needs, and long-term objectives. When applied thoughtfully, it creates a disciplined investment framework that reduces emotional decision-making and supports consistency across market cycles, while still allowing for customization based on individual circumstances.

Age-based portfolio allocation also serves as a communication tool between investors and advisors. It helps translate abstract risk concepts into a timeline that most people intuitively understand. Rather than debating short-term market forecasts, the focus stays on aligning capital with future needs. This long-term orientation is especially valuable in volatile markets, where reactive decisions often harm performance. By anchoring strategy to age and life stage, investors are more likely to maintain discipline, rebalance appropriately, and stay invested through periods of uncertainty. Over time, this structured approach can improve risk management and decision quality, even if exact allocations vary between individuals.

Why Age Matters for Investment Strategy

Age matters for investment strategy because it directly influences how much time an investor has to compound returns and absorb losses. A longer time horizon allows for greater exposure to volatile assets, since short-term drawdowns are less damaging when there is sufficient time for recovery. Younger investors can often prioritize growth because future earnings act as a form of human capital that offsets portfolio risk. As age increases, that human capital gradually converts into financial capital, increasing the importance of protecting accumulated assets rather than aggressively growing them.

Another reason age is central to strategy is that financial goals evolve over time. Early stages often focus on accumulation, career development, and long-term growth. Mid-career stages may involve competing priorities such as education costs, business investments, or real estate. Later stages emphasize income stability, healthcare planning, and longevity risk. Each phase places different demands on capital. Age provides a practical framework for anticipating these transitions and adjusting portfolio structure before changes become urgent. This proactive alignment reduces the likelihood of forced selling during unfavorable market conditions.

Age also affects psychological tolerance for risk. Even investors with strong analytical skills often experience declining comfort with volatility as portfolios grow larger and dependence on those assets increases. Losses feel more consequential when fewer working years remain to recover. Recognizing this behavioral reality is critical to designing a sustainable investment strategy. An allocation that looks optimal on paper but cannot be maintained emotionally will fail in practice. Age-aware strategies help align portfolio risk with both financial capacity and behavioral resilience, increasing the likelihood that investors stay committed to their plan over the long term.

How Time Horizon and Risk Tolerance Interact

Time horizon and risk tolerance are closely related but not interchangeable. Time horizon refers to how long capital can remain invested before it is needed. Risk tolerance reflects how much volatility an investor can emotionally and financially withstand. A long time horizon generally supports higher risk exposure, but it does not automatically imply high risk tolerance. Some investors with decades ahead still prefer stability, while others with shorter horizons may accept volatility due to strong income or external assets. Effective portfolio allocation requires understanding how these two factors interact rather than assuming they move together.

When time horizon is long, volatility becomes less threatening from a mathematical perspective because markets have historically rewarded patience. However, risk tolerance determines whether an investor can remain invested during inevitable downturns. If tolerance is low, even a theoretically optimal growth allocation can lead to poor outcomes if panic selling occurs. Conversely, a high risk tolerance with a short time horizon can expose an investor to sequence-of-returns risk, where early losses have an outsized impact on long-term results. Balancing these dynamics is essential to building a portfolio that performs well both financially and behaviorally.

The interaction between time horizon and risk tolerance also evolves with life events. Career changes, liquidity needs, or unexpected obligations can shorten effective time horizons overnight. Similarly, major gains or losses can permanently alter an investor’s perception of risk. This is why portfolio allocation should be reviewed periodically rather than set once. Age-based frameworks provide structure, but successful implementation depends on continuously aligning time horizon realities with true risk tolerance. When these elements are aligned, portfolios are more resilient, decision making improves, and long-term strategy remains intact across changing market conditions.

Classic Allocation Rules and Their Limitations

Advisors often point to simple rules like subtracting age from 100 or 120 to get the suggested stock allocation. These formulas are quick guides, not universal prescriptions.

The Rule of 100 and the Rule of 120

The “Rule of 100” suggests that your stock allocation should be 100 minus your age. A 40-year old would hold 60 percent stocks. Some modern variants use 110 or 120 to account for longer life spans and longer retirements.

Why Simple Formulas Help and Where They Fall Short

Simple formulas do not capture personal risk capacity, income needs, or other assets. They also ignore the role of bonds, alternatives, and cash equivalents in smoothing volatility.

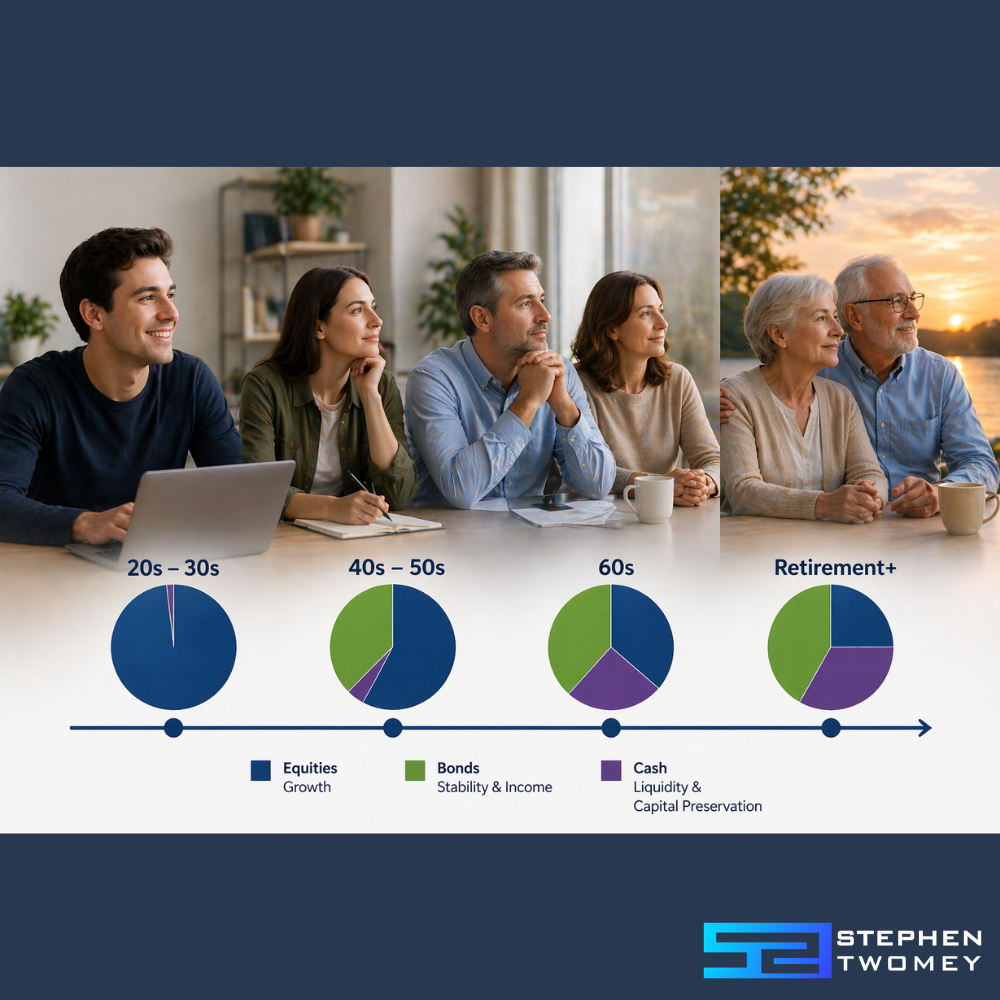

Recommended Allocation by Decade

Age-based portfolio allocation provides a structured way to align investment strategy with changing financial priorities, risk tolerance, and time horizon. While no allocation model fits every investor, decades of market data support the idea that portfolio composition should evolve as earning power, liquidity needs, and capital preservation become more relevant. The goal is not to time markets, but to manage risk intelligently while allowing capital to work efficiently over time. Each decade introduces different constraints and opportunities, which is why thoughtful adjustments matter more than rigid formulas.

In Your 20s: Growth and Compounding

Investors in their 20s typically have the longest time horizon, which makes growth the dominant objective. With decades before retirement, portfolios can absorb volatility and benefit from equity-driven compounding. A higher allocation to growth-oriented assets supports this goal, especially when paired with consistent contributions. The most important driver at this stage is not precision allocation, but participation and discipline. Market drawdowns are less threatening because time allows recovery. Investors can also afford to prioritize learning, experimentation, and building investment habits that support long-term consistency.

In Your 30s: Momentum and Balance

During the 30s, income often rises and financial responsibilities increase. While growth remains important, investors begin to balance opportunity with stability. Portfolios may still lean heavily toward growth assets, but diversification becomes more intentional. This is often the decade when investors introduce risk management tools, diversify across asset classes, and pay closer attention to downside exposure. The combination of rising cash flow and longer runway still supports growth, but decisions increasingly reflect competing priorities like family, housing, and liquidity needs.

In Your 40s: Peak Earning Years

The 40s are commonly peak earning years, which elevates the importance of protecting accumulated capital. While growth is still necessary, risk management becomes more prominent. Investors often shift toward a more balanced allocation that reduces exposure to severe market swings. This is also a period when portfolio structure matters more than raw returns. Strategic diversification, tax awareness, and rebalancing discipline can materially impact outcomes. Decisions made in this decade often set the foundation for retirement flexibility later.

In Your 50s: Preservation and Stability

In the 50s, the focus increasingly shifts toward capital preservation and volatility control. The margin for recovery from large losses narrows as retirement approaches. Allocations often emphasize stability, income potential, and reduced drawdown risk. Growth is still relevant, but it is no longer the primary objective. Investors may also prioritize liquidity planning and withdrawal strategy considerations. The emphasis is on protecting purchasing power while positioning the portfolio to support predictable future cash needs.

Age 60 and Beyond: Income and Legacy

After age 60, portfolios are typically structured to support income, longevity, and legacy goals. Capital preservation and sustainable withdrawals take priority over aggressive growth. Asset allocation decisions focus on managing sequence of returns risk, ensuring liquidity, and maintaining flexibility. For many investors, this stage also introduces estate and legacy planning considerations. The objective is to align the portfolio with real world cash flow needs while maintaining enough growth to address inflation and long term expenses.

Beyond Stocks and Bonds

Age-based allocation should not be limited to equities and fixed income. Alternatives and real assets may offer diversification and inflation protection. Private placements, real estate, infrastructure, and commodities can have a role. Including them requires careful risk assessment.

Real Assets, Private Equity, and Alternatives

Alternative investments can smooth portfolio volatility and improve risk adjusted returns. Accredited investors often gain access to these through private placements or niche funds.

Cash, HYSA, and Bond Substitutes

Cash and high-yield savings accounts can act as substitutes for traditional fixed income. They offer liquidity and safety, especially valuable during market downturns.

Rebalancing and Portfolio Management Practices

Asset allocation is not static. Markets cause drift. Rebalancing resets your target allocation periodically.

How Often to Review Allocation

Annual review is a minimum best practice. Major life events should prompt immediate review.

Tax Location and Efficiency

Tax efficient placement of assets can materially impact long-term after-tax returns. Placing high turnover or high yield assets in tax-advantaged accounts can enhance efficiency.

Common Allocation Mistakes and How to Avoid Them

Age-based portfolio allocation is a useful framework, but it is often misunderstood or applied too rigidly. Investors frequently rely on simplified rules without accounting for personal circumstances, market structure, or evolving asset classes. These mistakes can lead to unintended risk, missed growth, or unnecessary volatility over time. Understanding the most common allocation errors helps investors refine their strategy and maintain alignment between age, goals, and risk capacity.

Relying Too Heavily on Age Alone

One of the most common mistakes is treating age as the sole driver of allocation decisions. While age provides insight into time horizon, it does not reflect income stability, net worth, or liquidity needs. Two investors of the same age can have very different financial profiles and risk capacities. Avoid this mistake by using age as a starting reference, then layering in cash flow, career stage, and long-term objectives before finalizing allocation targets.

Applying Simplistic Rules Without Context

Rules such as “100 minus age” or “120 minus age” are often followed without deeper analysis. These formulas can oversimplify complex realities like market volatility, interest rate environments, and alternative asset exposure. They are helpful benchmarks, not prescriptions. Investors should treat these rules as rough guides, then adjust allocations based on personal tolerance for drawdowns and expected holding periods.

Ignoring Portfolio Drift Over Time

Many investors set an allocation once and fail to revisit it. Market performance naturally causes portfolios to drift, often increasing risk exposure during long bull markets. This can leave older investors with more equity risk than intended. Regular reviews and disciplined rebalancing help realign portfolios with age-based targets and reduce unintended concentration risk.

Excluding Non-Traditional Assets Without Evaluation

Many age-based models consider only stocks and bonds. This omission can limit diversification. Real assets, private investments, and alternative strategies may offer risk-adjusted benefits when sized appropriately. Avoiding them entirely due to familiarity bias can be a missed opportunity. Each asset class should be evaluated based on risk, liquidity, and correlation, not excluded by default.

Tools and Resources for Optimization

Professional dashboards, retirement calculators, and diversified index products are tools for refinement and tracking. Consider custom analytics that incorporate income streams and drawdown plans.

Conclusion

Age is a guide, not a rule. Alignment of time horizon, risk tolerance, and investment goals generates a resilient allocation strategy. This methodology supports long-term financial resilience and strategic performance.

Explore more insights on scaling businesses, building strategic partnerships, and navigating modern investment ecosystems at StephenTwomey.com.