Disclosure: none of the writing on this article or this site is financial advice.

401K plans give investors tax-advantaged growth on retirement savings. A frequent question concerns capital gains inside these accounts and how taxes apply.

What Are Capital Gains and How Do They Work in Retirement Accounts?

Capital gains are the profits earned when an asset is sold for more than its original purchase price. Common examples include stocks, mutual funds, exchange traded funds, real estate, and private investments. In taxable accounts, capital gains are typically divided into short term and long term categories. Short term gains apply to assets held for one year or less and are generally taxed at ordinary income tax rates.

Long term gains apply to assets held longer than one year and often benefit from lower preferential tax rates under current U.S. tax law. This distinction plays a major role in traditional investment planning because it influences when assets are sold, how portfolios are rebalanced, and how much tax is owed each year. Investors in taxable brokerage accounts must account for capital gains taxes annually, which can reduce net returns over time. This ongoing tax impact is often referred to as tax drag and can materially affect long term compounding, especially for actively managed portfolios or strategies that involve frequent trading.

In retirement accounts such as 401Ks and IRAs, capital gains function very differently. While investments inside these accounts still generate gains through price appreciation, those gains are not taxed at the time they occur. Instead, retirement accounts are structured to allow tax deferred or tax free growth depending on the account type. In a traditional 401K, capital gains accumulate without triggering annual taxes, allowing the full balance to compound over time.

Taxes are deferred until funds are withdrawn, at which point distributions are generally taxed as ordinary income rather than capital gains. In a Roth 401K, contributions are made with after tax dollars, but qualified withdrawals including all investment gains can be tax free. This structure removes annual capital gains taxation from the growth phase entirely and shifts the tax focus to the contribution or distribution stage. Understanding this difference is essential for retirement planning, asset allocation, and long term tax strategy.

Do You Pay Capital Gains Taxes in a 401K?

You do not pay capital gains taxes inside a 401K while your investments are growing. A 401K is a tax-advantaged retirement account, which means buying and selling assets within the account does not trigger taxable events in the year those trades occur. Stocks, mutual funds, ETFs, and other permitted investments can appreciate, generate dividends, or be rebalanced without creating capital gains liability. This structure allows the full value of the portfolio to remain invested, which can significantly enhance long-term compounding. In a taxable brokerage account, capital gains taxes can reduce returns over time as profits are partially paid out to the government each year.

In contrast, a 401K shields those gains during the accumulation phase. This tax deferral is one of the primary reasons retirement accounts are powerful wealth-building tools, particularly for investors with long time horizons. It also simplifies portfolio management since investors can rebalance without tax friction, allowing for more disciplined asset allocation decisions as markets change.

Taxes come into play when you begin withdrawing money from a 401K, and this is where many investors misunderstand capital gains treatment. Distributions from a traditional 401K are taxed as ordinary income, not as capital gains, regardless of how the growth was generated inside the account. Whether your balance grew through stock appreciation, dividends, or interest, the IRS treats withdrawals as income in the year received. This means the applicable tax rate depends on your income level at the time of withdrawal, not on capital gains tax brackets.

Roth 401K accounts operate differently. Contributions are made with after-tax dollars, and qualified withdrawals in retirement are generally tax-free, including all investment gains. This effectively eliminates future taxation on those gains if IRS rules are met. Understanding this distinction is critical for retirement tax planning, withdrawal timing, and decisions around Roth conversions.

Tax-Deferred Growth and Compounding Advantage

Because gains are not taxed as they occur, your full investment can continue to compound. This avoids what is sometimes called tax drag in taxable accounts. Tax drag can materially reduce long-term growth because annual gains are chipped away by taxes.

With tax deferral in a 401K, your money stays fully invested for decades, potentially boosting overall growth compared to a taxable account with similar returns.

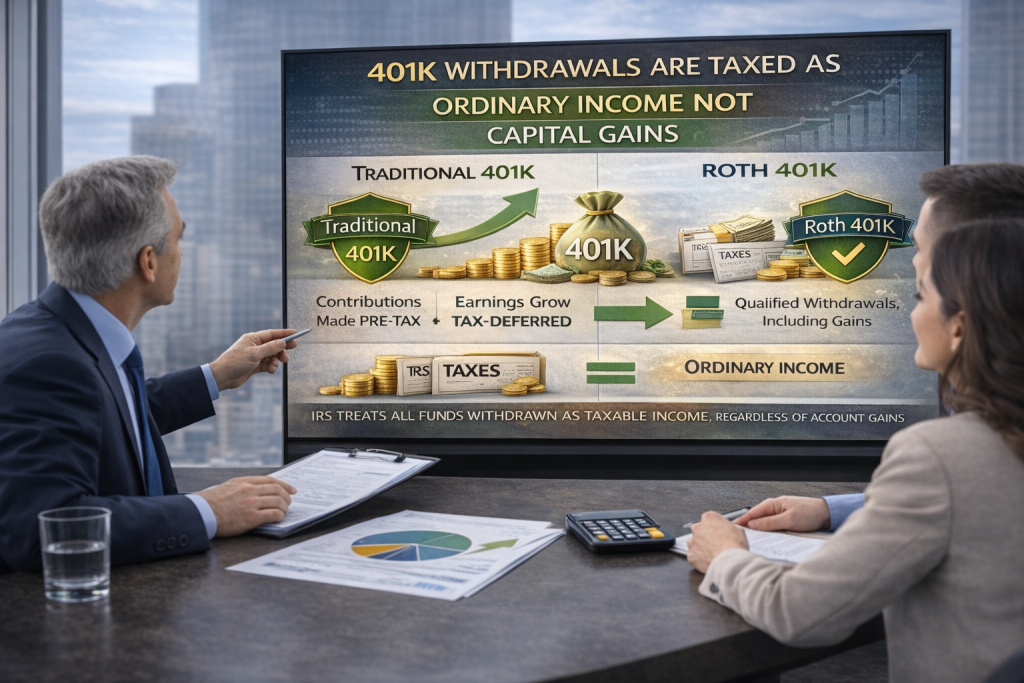

Are 401K Withdrawals Taxed as Ordinary Income or Capital Gains?

The key point for retirement planning is that distributions from a traditional 401K are taxed as ordinary income. The IRS treats all funds you withdraw as taxable income in the year of withdrawal. The Annuity Expert

This is true regardless of how the investments performed inside the account. Even if the growth came from capital gains, the withdrawal is taxed at your income tax rate.

Traditional 401K

Contributions are typically made pre-tax. Earnings and gains grow without annual tax. When you take money out in retirement, the full amount is taxed as ordinary income.

Roth 401K

Roth 401K contributions are made with after-tax dollars. Qualified withdrawals, including gains, are tax-free if rules on age and timing are met. This converts future capital gains into tax-free retirement income.

Strategic Tax Planning With 401K Accounts

Because traditional 401K withdrawals become ordinary income, thoughtful planning matters.

- Roth conversion can shift future growth into tax-free territory.

- Withdrawals timed across years may keep you in a lower bracket.

- Asset location puts high-growth investments in tax-advantaged accounts to maximize compounding. Wikipedia

Pairing 401K planning with after-tax accounts allows you to retain some of the preferential capital gains tax structure outside retirement accounts.

Practical Examples

Imagine two $100,000 portfolios over 20 years. One is in a taxable account and one in a 401K. Both earn the same returns annually. The taxable account loses some gains each year to capital gains or dividend taxes. The 401K retains all growth until withdrawal. Over time, that difference compounds.

When funds are eventually withdrawn from the 401K, the tax owed may be lower or higher than capital gains tax, depending on your retirement income bracket.

Key Risks and Considerations for Accredited Investors

Early withdrawals before age 59½ may incur penalties and taxes. State tax laws can also impact retirement income taxes. Required minimum distributions (RMDs) apply to traditional 401Ks and can increase taxable income in later years.

Frequently Asked Questions

Q: Do I pay capital gains tax on a 401K investment sale inside the plan?

A: No, gains inside the plan are tax-deferred until distribution.

Q: Are withdrawals from a 401K subject to capital gains tax?

A: No, they are taxed as ordinary income.

Q: Does a Roth 401K eliminate taxes on gains?

A: Qualified Roth withdrawals are tax-free including gains.

Conclusion

401K capital gains grow tax-deferred, offering a powerful compounding advantage. The tax liability occurs at distribution and is treated as ordinary income in traditional plans. Savvy planning can align withdrawal timing and account types to optimize retirement tax outcomes.

For more insights on business development, capital growth strategies, and the evolving landscape of private markets, visit StephenTwomey.com — where strategy meets execution.