Investment management fees are a standard cost of building and maintaining a portfolio. For years, investors assumed at least part of those costs could be offset through tax deductions. Today, the rules are far less favorable, and understanding them is essential for effective wealth strategy.

This article explains how investment management fees are treated under current tax law, why the rules changed, and what accredited investors should consider when structuring portfolios.

Understanding Investment Management Fees

What Counts as an Investment Management Fee

Investment management fees include charges paid to financial advisors, portfolio managers, or registered investment advisors for managing assets. These fees may cover asset allocation, investment selection, reporting, and ongoing advice. They are typically calculated as a percentage of assets under management.

How These Fees Are Typically Charged

Most advisory fees are deducted directly from investment accounts on a quarterly or annual basis. Others may be billed separately. From a tax perspective, how and where the fee is paid can matter just as much as the amount.

Historical Tax Treatment of Investment Management Fees

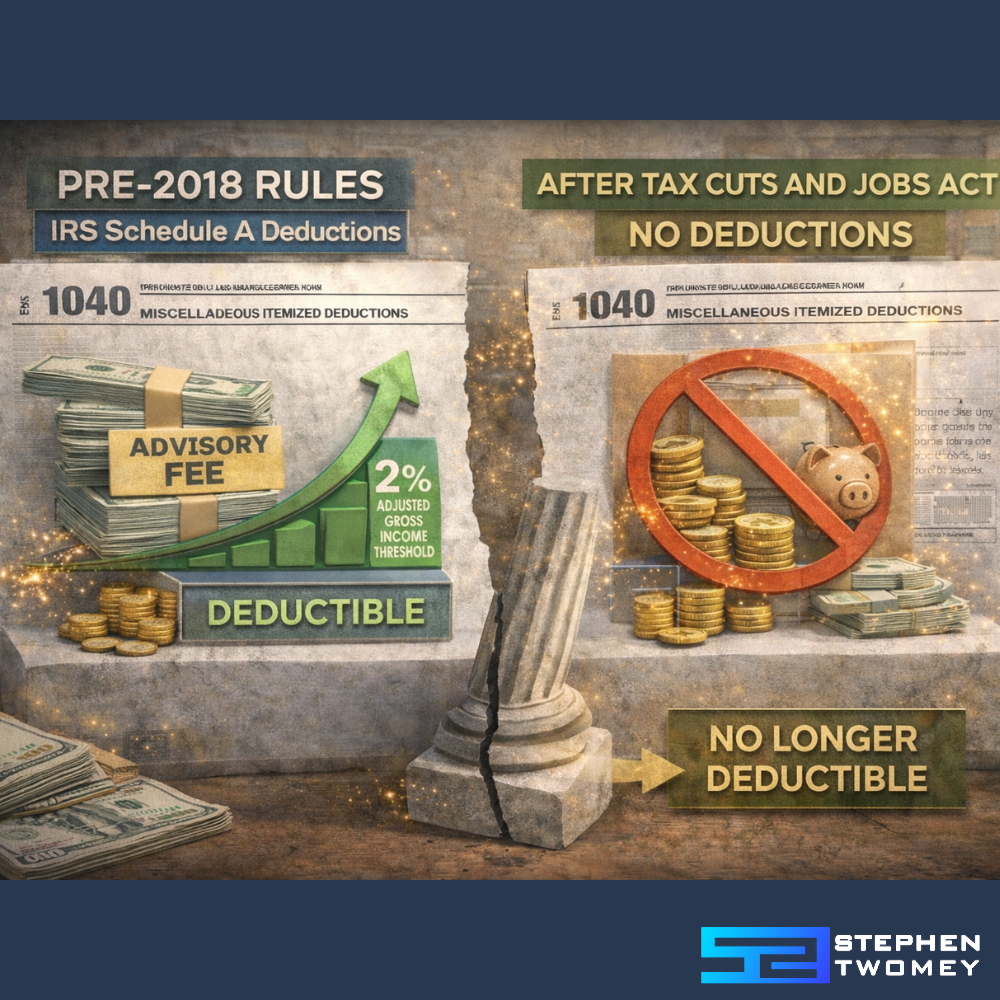

Pre-2018 IRS Rules and Schedule A Deductions

Before 2018, investment management fees were generally deductible as miscellaneous itemized deductions on Schedule A. They were subject to a 2 percent adjusted gross income threshold. This meant only the portion exceeding that limit could be deducted.

The Impact of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act eliminated all miscellaneous itemized deductions subject to the 2 percent rule. This change applied from 2018 through at least 2025. As a result, most individual investors lost the ability to deduct investment management fees entirely.

Are Investment Management Fees Tax Deductible Today?

The Current IRS Position

Under current IRS rules, investment management fees are not tax deductible for individual investors holding assets in taxable brokerage accounts. This applies regardless of income level, portfolio size, or fee structure.

Why Most Individual Investors Can No Longer Deduct Them

The elimination of these deductions was part of a broader effort to simplify the tax code. While standard deductions increased, specialized write-offs like investment fees were removed. According to Investopedia, this change disproportionately affected higher-income investors who previously itemized deductions.

Exceptions and Strategic Workarounds

Fees Inside Retirement Accounts

Investment management fees paid inside retirement accounts such as IRAs or 401(k)s are not deductible. However, they may be paid with pre-tax dollars in traditional accounts, which can soften the economic impact over time.

Business Entities, Trusts, and Estates

Certain trusts and estates may still deduct investment management fees if they are considered necessary for administration. The rules are complex and depend on how expenses are classified. Entity-level planning with a qualified CPA is essential.

Private Investments and Alternative Asset Structures

Accredited investors often hold assets through LLCs, partnerships, or private funds. In some cases, management fees may be treated as business expenses at the entity level. This does not create a personal deduction, but it can improve overall tax efficiency. This is especially relevant in private equity and hedge fund structures.

Implications for Accredited and High-Net-Worth Investors

Portfolio Construction and Fee Location

For sophisticated investors, the focus shifts from deductibility to optimization. Placing higher-fee strategies inside tax-advantaged or entity-based structures can reduce friction. Fee location has become as important as asset location.

Coordinating Investment and Tax Strategy

Investment decisions should not be made in isolation from tax planning. Advisors, CPAs, and legal professionals must coordinate. Without alignment, investors may unknowingly erode after-tax returns.

Practical Takeaways for Investors

Questions to Ask Your Advisor and CPA

Ask where your fees are being paid, how they are classified, and whether entity structures could improve efficiency. Do not assume past tax treatment still applies. Rules have changed, and strategies must adapt.

Planning Ahead for Regulatory Changes

Tax law is not static. The current rules are scheduled for review after 2025. Investors who stay informed and flexible will be better positioned to respond.

Conclusion

Investment management fees are no longer tax deductible for most individual investors. For accredited investors, however, planning opportunities still exist through entity structures, alternative assets, and coordinated strategy. The key is understanding the rules and designing portfolios with after-tax outcomes in mind.

For in-depth analysis on private market dynamics, business strategy, and capital formation, visit StephenTwomey.com for ongoing research and commentary.

Disclosure: None of the information provided in this article or on this site constitutes financial, tax, or investment advice. Always consult qualified professionals regarding your specific situation.