What Is a Market Neutral Strategy?

A market neutral strategy is an investment approach designed to reduce or eliminate exposure to overall market movements by balancing long and short positions.

Instead of attempting to predict whether markets will rise or fall, market neutral traders aim to profit from relative price movements between securities.

The core objective is simple:

- Minimize broad market risk

- Generate returns from pricing inefficiencies

- Reduce portfolio volatility

Market neutral investing is widely used by:

- Hedge funds

- Quantitative trading firms

- Institutional investors

- Proprietary trading desks

Unlike traditional investing, where performance is heavily influenced by market direction, market neutral portfolios attempt to remain insulated from broad market swings.

This makes market neutral investing a core component of many advanced quantitative trading strategies.

How Market Neutral Trading Works

Market neutral trading works by simultaneously holding long and short positions in related assets.

The goal is to isolate relative performance while minimizing systematic market exposure.

For example:

- Long undervalued stock

- Short overvalued stock

If both stocks rise because of a bullish market, gains and losses may offset each other. The portfolio profits only if the long position outperforms the short position.

This structure makes market neutral strategies highly attractive during volatile or uncertain market conditions.

Long/Short Equity Structure

The most common form of market neutral investing is long/short equity.

The process typically involves:

- Identifying undervalued securities

- Identifying overvalued securities

- Buying undervalued assets

- Short selling overvalued assets

For example:

- Long Microsoft

- Short another overvalued technology stock

The strategy profits if Microsoft outperforms the short position regardless of overall market direction.

Long/short equity systems are commonly used by:

- Quant hedge funds

- Fundamental hedge funds

- Statistical arbitrage desks

Many institutional hedge funds vs quant funds comparisons focus heavily on how market neutral strategies are implemented differently across firms.

Beta Neutral vs Dollar Neutral

Not all market neutral strategies are structured the same way.

Two common approaches are:

- Beta neutral

- Dollar neutral

Dollar Neutral

Dollar neutral portfolios balance capital equally between long and short positions.

Example:

- $1 million long exposure

- $1 million short exposure

This reduces directional market exposure.

However, equal dollar exposure does not necessarily eliminate volatility risk because securities may have different sensitivities to market movements.

Beta Neutral

Beta neutral portfolios adjust positions based on beta rather than capital size.

Beta measures how sensitive an asset is to market movements.

β=Cov(ri,rm)Var(rm)\beta = \frac{Cov(r_i, r_m)}{Var(r_m)}β=Var(rm)Cov(ri,rm)

In beta neutral investing:

- Higher-beta stocks receive smaller allocations

- Lower-beta stocks may receive larger allocations

The objective is to minimize correlation with overall market returns.

Beta neutral systems are common in sophisticated quant trading strategies because they provide better risk-adjusted exposure.

Types of Market Neutral Strategies

Market neutral investing includes a wide range of quantitative and systematic approaches.

Some focus on pricing inefficiencies, while others focus on factor exposures or relative value opportunities.

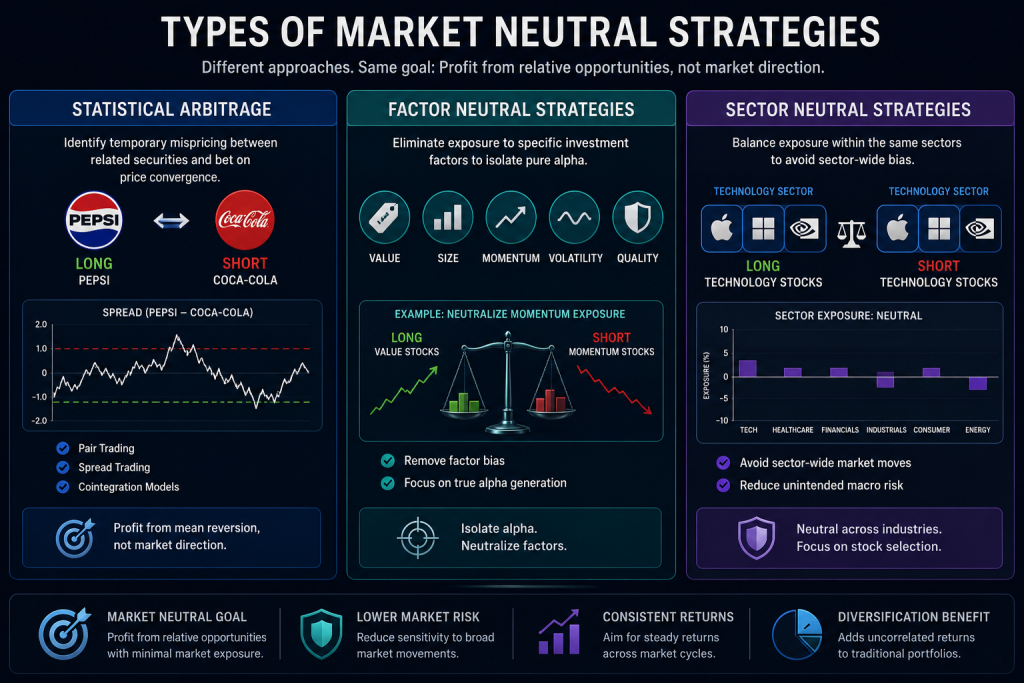

Statistical Arbitrage

Statistical arbitrage is one of the most popular forms of market neutral trading.

These strategies identify temporary mispricing between related securities and bet on price convergence.

Common examples include:

- Pair trading

- Spread trading

- Cointegration models

For example:

- Long Pepsi

- Short Coca-Cola

If the spread between the two stocks normalizes, the trade profits regardless of whether the overall market rises or falls.

This type of strategy is central to advanced statistical arbitrage strategies used by institutional quant firms.

Factor Neutral Strategies

Factor neutral investing attempts to eliminate exposure to specific investment factors.

Common factors include:

- Value

- Size

- Momentum

- Volatility

- Quality

For example:

- A portfolio may neutralize momentum exposure while targeting value opportunities

This approach attempts to isolate pure alpha generation rather than factor-driven returns.

Large quantitative firms often use factor neutral systems within multi-factor portfolios and broader quantitative trading frameworks.

Sector Neutral Strategies

Sector neutral investing balances exposure across industries.

For example:

- Long technology stocks

- Short technology stocks

rather than:

- Long technology

- Short energy

This prevents sector-wide movements from distorting performance.

Sector neutrality is especially important during periods of macroeconomic stress when industries move together.

Market Neutral Quant Funds

Many quantitative hedge funds operate fully market neutral portfolios.

These systems rely on:

- Machine learning

- Statistical models

- High-frequency execution

- Factor optimization

Firms like:

- AQR

- Two Sigma

- Renaissance Technologies

have historically used market neutral approaches within broader systematic investment strategies.

Benefits of Market Neutral Trading

Market neutral strategies offer several advantages compared to traditional long-only investing.

Reduced Exposure to Market Crashes

Because long and short positions offset market exposure, market neutral portfolios can perform better during:

- Bear markets

- Volatility spikes

- Financial crises

This risk reduction is one reason institutional investors allocate capital to market neutral hedge funds.

Lower Portfolio Volatility

Market neutral systems often experience:

- Smaller drawdowns

- More stable returns

- Reduced directional risk

This makes them attractive for diversification.

Consistent Return Potential

Rather than depending entirely on bull markets, market neutral strategies attempt to generate returns through:

- Relative pricing inefficiencies

- Statistical edges

- Factor dislocations

This allows performance across multiple market regimes.

Diversification Benefits

Market neutral strategies often have low correlation with traditional equity portfolios.

As a result, institutional investors use them to improve portfolio diversification.

This is particularly important for pension funds and endowments seeking smoother long-term performance.

Risks of Market Neutral Strategies

Although market neutral investing reduces market exposure, it still carries substantial risks.

Model Risk

Quantitative models rely on historical relationships that may break down unexpectedly.

Changes in:

- Volatility

- Correlation

- Market structure

can significantly damage performance.

Short Squeeze Risk

Short positions carry unique risks.

If heavily shorted securities rise rapidly:

- Losses can become unlimited

- Forced covering can accelerate price increases

Short squeezes have caused major losses for hedge funds in recent years.

Execution Costs

Market neutral systems often require frequent trading.

This creates costs including:

- Slippage

- Bid-ask spreads

- Borrow fees

- Commissions

Execution quality becomes critically important in modern algorithmic trading environments.

Liquidity Risk

In stressed markets, liquidity can disappear quickly.

This makes it difficult to:

- Exit positions

- Maintain hedges

- Control volatility

Liquidity risk is particularly dangerous for leveraged market neutral portfolios.

When Market Neutral Strategies Perform Best

Market neutral systems often perform best during:

- Volatile markets

- Sideways markets

- Uncertain macro environments

- High-dispersion stock markets

When individual stock performance diverges significantly, relative value opportunities increase.

However, market neutral systems may struggle during:

- Strong momentum-driven bull markets

- Sudden factor rotations

- Extreme market dislocations

This is why many firms combine market neutral investing with broader quant trading strategies.

FAQ: Do Market Neutral Strategies Make Money in Bear Markets?

Yes. Market neutral strategies are designed to generate returns regardless of overall market direction.

Because they balance long and short positions, profits depend more on relative asset performance than on whether markets rise or fall.

This makes market neutral investing particularly attractive during:

- Bear markets

- Recessions

- Volatile environments

However, performance still depends on:

- Model quality

- Risk management

- Execution efficiency

FAQ: Who Uses Market Neutral Strategies?

Market neutral strategies are widely used by:

- Hedge funds

- Quantitative trading firms

- Institutional investors

- Proprietary trading firms

These organizations use market neutral systems to:

- Reduce volatility

- Diversify portfolios

- Generate risk-adjusted returns

Many of the world’s largest quantitative trading firms incorporate market neutral investing into broader systematic portfolios.