Most 401K plans are built around public stocks and bonds. That structure worked well for decades, but market concentration, inflation risk, and volatility have pushed many investors to explore broader options. 401K investment alternatives offer a way to diversify beyond traditional allocations while aligning with long term retirement goals.

Why Investors Are Looking Beyond Traditional 401K Allocations

Traditional 401K portfolios were designed for a different market environment. For decades, a mix of public equities and bonds delivered acceptable returns with manageable volatility. That framework is now under pressure. Structural changes in markets, monetary policy, and asset correlations have reduced the effectiveness of conventional diversification. As a result, many investors are reassessing how their retirement capital is allocated and questioning whether standard 401K menus still align with long term wealth preservation and growth goals.

1. Increased Market Concentration and Equity Risk

One of the primary drivers is the growing concentration risk within public equity markets. Major indices are now heavily weighted toward a small number of large technology companies, which exposes investors to sector specific downturns even when they believe they are diversified. In many 401K plans, equity exposure is further amplified through target date funds and index heavy lineups. This creates a situation where retirement outcomes are tied closely to the performance of a narrow slice of the market. When volatility rises or valuations compress, portfolios can experience sharper drawdowns than expected. Investors who understand risk at a portfolio level are increasingly aware that diversification across asset classes does not always translate to diversification across risk factors. This realization has pushed them to explore assets whose performance drivers are not linked to public market sentiment or index composition.

2. Bonds No Longer Provide the Same Risk Buffer

Bonds have traditionally served as the stabilizing force in 401K portfolios. However, extended periods of low interest rates followed by rapid tightening have challenged that role. Rising rates can reduce bond prices, while inflation erodes real returns. During recent market cycles, stocks and bonds have at times declined simultaneously, undermining the core assumption of negative correlation. For retirement investors relying on bonds to dampen volatility and preserve capital, this shift has been unsettling. Many now recognize that fixed income alone may not offer sufficient protection against inflation or systemic risk. This has led to greater interest in alternative assets that may provide income, inflation sensitivity, or contractual cash flows. The goal is not to abandon bonds entirely, but to supplement them with strategies that behave differently under changing macroeconomic conditions.

3. Demand for True Diversification and Long Term Value Creation

A growing number of investors are focused on how wealth is actually created over long time horizons. Traditional 401K investments are largely driven by market pricing and short term liquidity. Alternative investments, by contrast, often emphasize operational improvement, asset ownership, or private market inefficiencies. This distinction appeals to investors who want exposure to returns generated through business growth, cash flow, or real asset appreciation rather than daily market fluctuations. Additionally, institutional investors such as pensions and endowments have long used alternatives to improve risk adjusted returns. Individual investors are increasingly seeking similar tools within their retirement strategies. While alternatives introduce complexity and illiquidity, many investors view these as acceptable tradeoffs for broader diversification and alignment with long term financial objectives.

Understanding What Qualifies as a 401K Investment Alternative

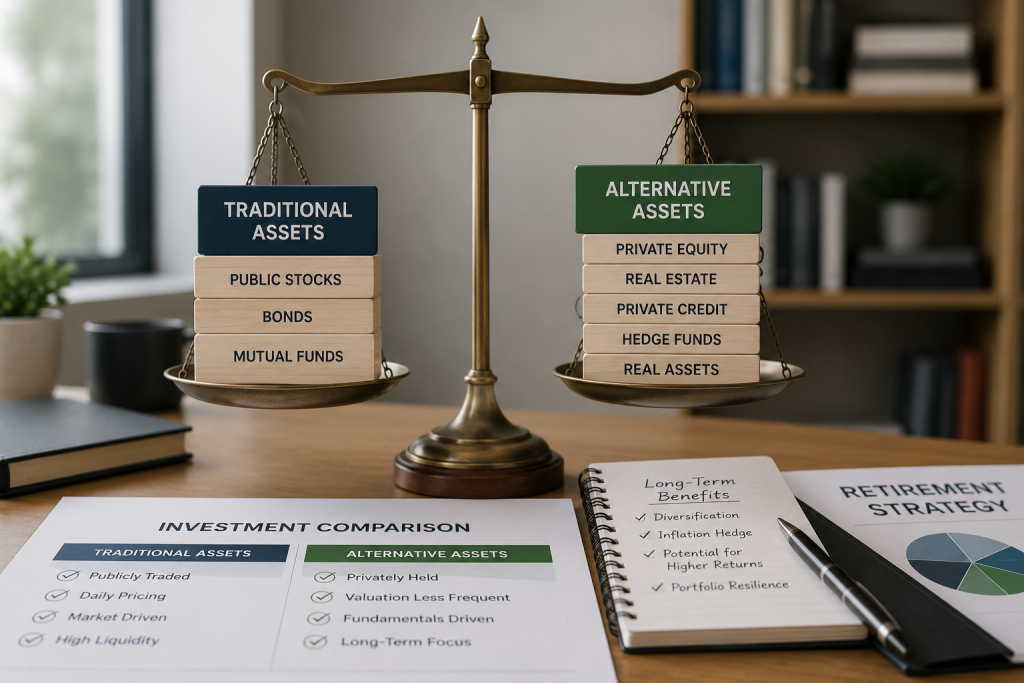

Traditional vs Alternative Assets Inside Retirement Plans

Traditional assets include publicly traded stocks, bonds, and mutual funds. Alternative investments typically include private equity, real estate, private credit, hedge funds, and real assets. These assets are not priced daily and often rely on long term value creation.

The distinction matters because alternatives behave differently across market cycles. They often prioritize cash flow, asset backing, or operational growth instead of market sentiment.

What Retirement Plans Allow Alternative Exposure

Not all 401Ks allow alternatives directly. Employer sponsored plans usually limit choices to pre selected funds. Self directed 401Ks and certain solo 401Ks expand the investment universe significantly, subject to IRS and ERISA rules.

Common 401K Investment Alternatives Explained

Private Equity and Private Placements

Private equity focuses on acquiring or investing in privately held companies. These investments target operational improvements and long term growth rather than short term price movements. In retirement accounts, access is typically limited to self directed structures and accredited investors.

Private placements may include growth equity, venture capital, or private credit. These assets introduce illiquidity but often compensate investors through higher expected returns and lower correlation to public markets.

Real Estate and Real Asset Exposure

Real estate is one of the most commonly used alternative investments in retirement strategies. It provides income potential and inflation sensitivity. Real assets such as infrastructure and energy assets can also serve as long term value stores.

Within a 401K structure, exposure may come through private real estate funds or direct ownership using self directed plans.

Hedge Funds and Absolute Return Strategies

Hedge funds use flexible strategies that can include long and short positions, derivatives, and arbitrage. The goal is often capital preservation and risk adjusted returns rather than market tracking.

While complex, these strategies can play a stabilizing role when public markets experience drawdowns.

Commodities and Inflation Sensitive Assets

Commodities and hard assets respond directly to supply and demand dynamics. They often perform well during inflationary periods when financial assets struggle. Exposure may come through managed funds rather than direct ownership.

How Self Directed 401Ks Expand Alternative Investment Access

Regulatory Structure and Custodian Requirements

Self directed 401Ks operate under the same tax rules as traditional plans but allow broader investment choices. A qualified custodian is required, and prohibited transaction rules must be followed carefully.

Investors must understand disqualified persons and avoid self dealing. Compliance is critical, especially when investing in private assets.

Risk Management and Compliance Considerations

Alternative investments introduce complexity. Valuation is less frequent, liquidity is limited, and due diligence requirements are higher. These risks can be managed through diversification, professional guidance, and conservative allocation sizing.

Benefits and Tradeoffs of Using Alternative Investments in a 401K

Portfolio Diversification and Correlation Reduction

Alternatives can reduce dependence on public market performance. Many private assets generate returns through cash flow, asset appreciation, or operational efficiency. This helps smooth portfolio volatility over time.

Institutional investors have used alternatives for decades to manage risk across cycles.

Liquidity, Valuation, and Complexity Risks

Illiquidity is the primary tradeoff. Capital may be locked up for years. Valuations are less transparent, and investment structures are more complex. These factors require patience and a long time horizon.

Who Should Consider 401K Investment Alternatives

Accredited Investors and Business Owners

Accredited investors often have access to private placements and specialized funds. Business owners may also benefit from solo 401K structures that allow greater control over asset selection.

These investors typically have higher risk tolerance and longer investment horizons.

High Income Professionals with Long Time Horizons

Professionals in medicine, law, and technology often face concentrated income risk tied to public markets. Alternative investments can help balance that exposure and support long term retirement planning.

Strategic Takeaways for Building a Modern Retirement Portfolio

A modern 401K strategy looks beyond traditional asset classes. It focuses on economic exposure, correlation, and long term value creation. Alternative investments are not replacements for public assets, but complements when used thoughtfully.

For more insights on business development, capital growth strategies, and the evolving landscape of private markets, visit StephenTwomey.com — where strategy meets execution.

Disclosure:

None of the content on this article or site constitutes financial, investment, or legal advice. Investors should consult qualified professionals before making investment decisions.