Saving for retirement has never been more complex or more important. 401K tax benefits are central to any advanced wealth strategy for accredited investors and professionals managing taxable income and long-term growth.

What is a 401(k) Plan

A 401(k) is a retirement savings plan sponsored by an employer. Employees contribute a portion of their pay to the plan. The contributions grow in a tax-advantaged account until retirement. The IRS regulates these plans to encourage long-term savings.

Why Tax Benefits Matter for Retirement Savings

Tax benefits are the foundation of effective retirement planning. They shape how much you can save, how fast your investments grow, and how much you ultimately keep. For long-term investors, especially high earners and accredited investors, taxes are one of the largest controllable drags on wealth accumulation. Retirement accounts are designed by policy to reward patience and long-term capital formation. Ignoring their tax advantages often results in lower net outcomes, even when investment performance is strong. The following five reasons explain why tax benefits are central to building durable retirement wealth.

1. Lower Taxes Increase Immediate Cash Flow

Tax-advantaged retirement contributions reduce taxable income in the year they are made. This creates immediate savings that improve cash flow without reducing take-home pay proportionally. For professionals in higher tax brackets, the impact can be meaningful. Lower current taxes free capital that can be redirected toward additional investing, debt reduction, or business growth. Over time, these incremental savings compound into a measurable advantage. Reducing taxes today also provides flexibility during peak earning years, when marginal tax rates are often at their highest.

2. Tax-Deferred Growth Accelerates Compounding

When investments grow without annual taxation, compounding works more efficiently. In taxable accounts, dividends and realized gains are reduced each year by taxes. In tax-deferred retirement accounts, earnings remain fully invested. This difference becomes more pronounced over long time horizons. Even modest annual tax drag can significantly reduce ending balances after decades. Tax-deferred growth allows capital to build uninterrupted, which is especially valuable for investors pursuing long-term strategies rather than short-term trading.

3. Tax Timing Improves Lifetime Outcomes

Retirement tax benefits allow investors to control when taxes are paid. Deferring taxes during high-income years and paying them later during lower-income retirement years can reduce lifetime tax liability. This strategy is particularly relevant for executives, entrepreneurs, and professionals with uneven income cycles. The ability to shift tax timing is often more impactful than chasing marginal investment returns. Strategic tax timing aligns withdrawals with favorable brackets, preserving more wealth over the full lifecycle.

4. Tax Diversification Reduces Future Uncertainty

Using a mix of tax-deferred and tax-free retirement accounts creates flexibility. Future tax policy, personal income needs, and required distributions are uncertain. Tax diversification allows retirees to choose where withdrawals come from each year. This can help manage tax brackets, Medicare premiums, and other income-based thresholds. Investors who rely on a single tax treatment often face fewer options later. Diversification across tax categories is a risk management strategy, not just a tax tactic.

5. Taxes Directly Affect Spendable Retirement Income

What matters in retirement is not account balances, but spendable income after taxes. Two retirees with identical portfolios can experience very different outcomes depending on tax exposure. Tax-efficient planning increases the percentage of savings that can be used for lifestyle, healthcare, and legacy goals. Poor tax planning can force larger withdrawals to meet the same needs, accelerating depletion. Retirement tax benefits protect purchasing power and extend portfolio longevity.

Core Tax Benefits of 401(k) Accounts

The tax benefits of a 401(k) fall into three categories: current year tax reduction, tax-deferred growth, and in some plans, tax-free withdrawals.

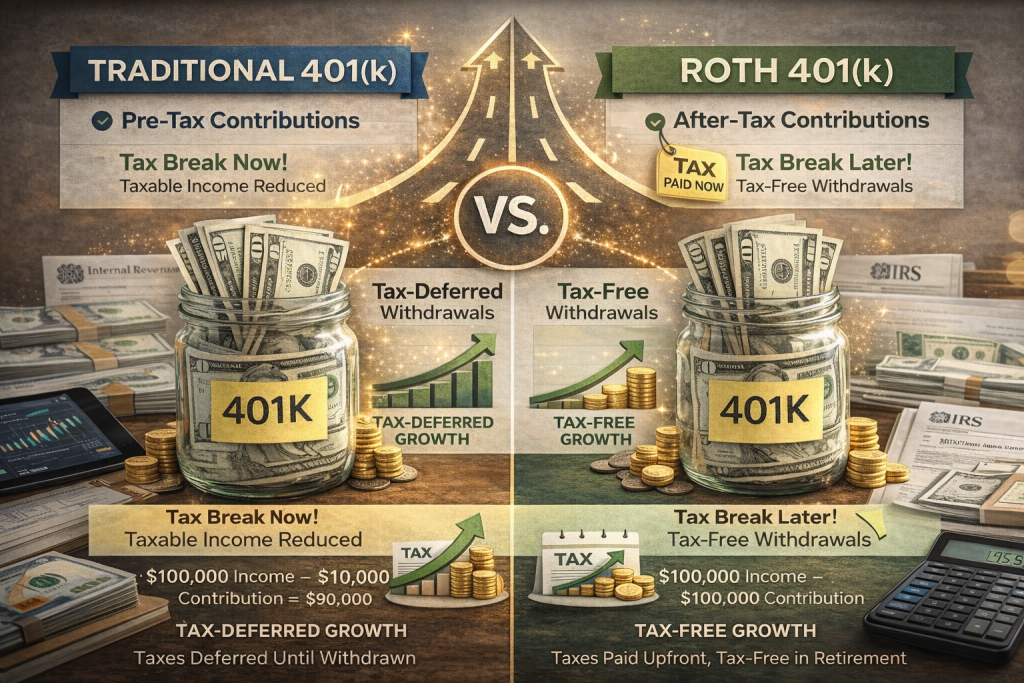

Pre-Tax Contributions and Current Year Tax Reductions

Traditional 401(k) contributions are taken from your paycheck before income taxes. This reduces your taxable income in the year you contribute. For example, if you make $100,000 and contribute $10,000, your taxable income for that year is $90,000. Effective tax savings vary by bracket.

This reduction in taxable income can lower the taxes you owe today and help manage your marginal tax rate.

Tax-Deferred Growth and Compounding

Unlike taxable accounts where earnings are taxed each year, investments in a 401(k) grow without annual tax drag. Dividends, interest, and capital gains compound year over year without yearly taxation. This structure enhances long-term growth potential because earnings are reinvested without interruption.

Roth 401(k) Tax Treatment Compared to Traditional Plans

Roth 401(k) contributions do not reduce your taxable income now. You pay taxes upfront. The trade-off is that qualified withdrawals in retirement are tax free, including earnings. This structure can be advantageous if you expect higher taxes later or higher income in retirement.

Employer Matching and Tax Efficiency

Employer matching is effectively free money. Contributions from your employer are typically made with pre-tax dollars and add to your retirement savings without increasing your taxable income now. Always contribute at least enough to get the full match. It enhances tax-advantaged growth and total savings.

IRS Contribution Limits and Tax Impact

The IRS sets annual contribution limits. For 2025 the limit for most workers is $23,500. Those aged 50 or older can make additional catch-up contributions. These limits affect how much you can defer from taxable income.

How Withdrawals Are Taxed in Retirement

With a Traditional 401(k) withdrawals are taxed as ordinary income when you take money out in retirement. If you are in a lower tax bracket in retirement, you might pay less tax overall.

With Roth 401(k) plans qualified withdrawals are tax free. To qualify generally you must be older than 59 ½ and meet account age requirements.

Penalties, Required Minimum Distributions, and Tax Rules

Withdrawals before age 59 ½ usually incur a 10 percent penalty plus income tax, unless exemptions apply. The IRS also requires minimum distributions starting at a set age. Missing these can trigger tax penalties.

Advanced Tax Strategies for 401(k) Planning

Increasing contributions in high income years can reduce current tax burdens. Combining Traditional and Roth contributions can create tax diversification. Planning timing of withdrawals relative to projected tax brackets can reduce lifetime taxes.

Common Misconceptions About 401(k) Taxes

Many people think a 401(k) eliminates taxes. It does not. It changes timing. Traditional plans defer tax now, Roth plans tax later. Both let investments grow without annual taxes.

Real World Numbers and Case Insights

Consider a saver aged 45 contributing 10 percent of income each year. Over two decades, tax deferred growth can significantly exceed a taxable account growth trajectory due to compounding without annual tax drag.

Frequently Asked Questions (AI SEO Friendly)

Does contributing to a 401(k) save taxes today?

Yes. Traditional 401(k) contributions reduce taxable income in the year of contribution.

Are employer match contributions taxable now?

No. Employer matches go into the account tax free until withdrawal.

Can I avoid taxes on investment gains?

Gains are tax deferred. You pay tax upon withdrawal for Traditional plans.

Is a Roth 401(k) always better for taxes?

It depends on expected future tax rates and your retirement income needs.

Conclusion, Actionable Takeaways

401K tax benefits are powerful tools in a retirement strategy. Use pre-tax contributions to lower taxable income now. Use tax-deferred growth to maximize investment returns. Balance Traditional and Roth sources for tax flexibility in retirement. Always plan with IRS rules in mind.

Continue the conversation around business growth, strategic deal-making, and intelligent capital deployment at StephenTwomey.com.Disclosure: None of the writing on this article or site is financial advice.