A Self-Directed IRA offers investors more control than traditional retirement accounts. It allows access to alternative assets that can generate consistent income over time. For investors focused on retirement cashflow, this structure can be powerful when used correctly.

This guide explains how to use a Self-Directed IRA strategically, not speculatively, with a focus on income, risk management, and long-term planning.

What is a Self-Directed IRA (SDIRA)

A Self-Directed IRA is a retirement account that allows investments beyond stocks, bonds, and mutual funds. The account remains tax-advantaged but shifts investment decisions to the account holder.

How SDIRAs Differ From Traditional IRAs

Traditional IRAs limit asset selection. SDIRAs expand it. Investors can allocate capital into real estate, private credit, and private businesses while maintaining IRA tax treatment.

The custodian administers the account but does not evaluate investments. Responsibility shifts to the investor.

Why Sophisticated Investors Use SDIRAs

Experienced investors use SDIRAs to align retirement capital with real-world deal flow. This includes assets they already understand. Control and flexibility are the primary drivers.

Why SDIRAs Are Powerful for Retirement Cashflow

The value of an SDIRA lies in how income is treated. Cashflow generated inside the account is not taxed annually.

Tax-Deferred vs Tax-Free Cashflow

In a Traditional SDIRA, income compounds tax-deferred. In a Roth SDIRA, qualified income can be tax-free. This accelerates long-term growth when income is reinvested.

According to IRS guidance in Publication 590, properly structured income retains its tax-advantaged status.

Control, Flexibility, and Asset Selection

Cashflow strategies are limited in public markets. SDIRAs unlock assets designed for income first. This includes rent, interest payments, and structured distributions.

Asset Types That Generate Cashflow Inside an SDIRA

Not all alternative assets are equal. Cashflow consistency matters more than headline returns.

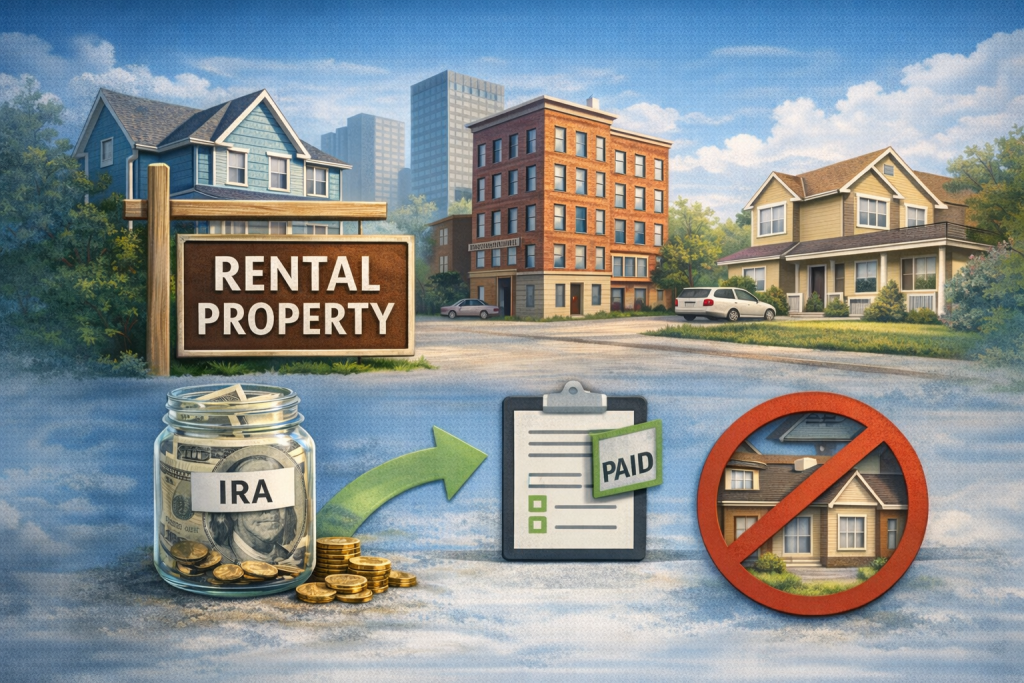

Real Estate and Rental Income

Rental properties are one of the most common SDIRA investments. All income flows back into the IRA. Expenses are paid from the IRA as well.

Investors must avoid personal use. Even minor violations can disqualify the account.

Private Lending and Promissory Notes

Private credit offers predictable income. Notes can pay monthly or quarterly interest directly into the IRA. This structure appeals to income-focused investors.

Risk assessment is critical. Underwriting matters more than yield.

Private Equity, Funds, and Syndications

Some private funds distribute cashflow during the hold period. Others focus on appreciation. Investors should review distribution policies closely.

Syndications can provide scale but introduce complexity.

How to Structure Cashflow Strategies Inside an SDIRA

Income without planning creates friction. Structure determines outcomes.

Income Timing and Liquidity Planning

Required minimum distributions can create forced liquidity. Investors should model future income needs early. Illiquid assets create challenges later.

Staggered maturities help manage this risk.

Reinvestment vs Distribution Decisions

Reinvested cashflow compounds faster. Distributions reduce future growth. The correct balance depends on age, tax structure, and retirement timeline.

SDIRA Rules, Risks, and Prohibited Transactions

Compliance risk is the most common SDIRA failure point.

Disqualified Persons Explained

The IRS prohibits transactions with certain related parties. This includes the account holder, spouses, and direct ancestors or descendants.

Violations can trigger immediate taxation and penalties.

Common Compliance Mistakes to Avoid

Using personal funds, providing services, or informal asset use are frequent errors. Documentation and discipline matter.

Custodians, Platforms, and Administrative Considerations

Custodians enable access but add friction.

Choosing the Right SDIRA Custodian

Not all custodians support the same assets. Fee structures vary widely. Service quality impacts execution speed.

Due diligence on custodians is as important as asset selection.

Fees, Reporting, and Operational Friction

SDIRAs involve setup fees, asset fees, and transaction fees. These reduce net returns. Investors should model fees over time.

When an SDIRA Makes Sense and When It Does Not

SDIRAs are not universal solutions.

Ideal Investor Profiles

SDIRAs fit investors with alternative asset experience. They work best for those seeking income, control, and tax efficiency.

They are often used by entrepreneurs and accredited investors.

Situations Where SDIRAs Underperform

Small account balances struggle with fees. Passive investors without deal access may underperform public markets.

Complexity is a real cost.

Strategic Takeaways for Long-Term Retirement Cashflow

A Self-Directed IRA is a framework, not a shortcut. When aligned with income-producing assets, it can support long-term retirement cashflow.

The key is discipline, compliance, and realistic expectations.

For a deeper understanding of alternative asset strategies, visit StephenTwomey.com.

For additional regulatory context, refer to IRS Publication 590 at IRS.gov.

Disclosure: This article is for educational purposes only. None of the content on this article or on StephenTwomey.com constitutes financial, legal, or investment advice.

For more insights on business development, capital growth strategies, and the evolving landscape of private markets, visit StephenTwomey.com — where strategy meets execution.