Investment strategies by age provide a framework for aligning financial decisions with life stages, risk capacity, and long term goals. While age alone should never dictate portfolio choices, it strongly influences time horizon, income stability, and capital needs. Understanding how strategy evolves over time leads to better outcomes and fewer costly mistakes.

Why Age Matters in Investment Strategy

Age plays a meaningful role in shaping investment strategy, but not in the simplistic way often described in mainstream advice. For accredited investors, age interacts with capital scale, access to private markets, and portfolio complexity. Life stage influences how risk is absorbed, how long capital can remain invested, and how aggressively alternative assets can be deployed. The following factors explain why age remains a strategic consideration, even for sophisticated investors.

Time Horizon and Capital Lockup

Age directly affects how long capital can remain invested without creating liquidity pressure. Younger accredited investors can tolerate longer lockup periods common in private equity, venture capital, and certain real asset strategies. These structures reward patience through illiquidity premiums and operational value creation. Older investors often shorten their effective time horizon, even if net worth remains high. That shift makes capital duration a central constraint rather than an abstract planning variable.

Risk Capacity Versus Portfolio Volatility

Risk capacity changes with age as income stability, business exposure, and reliance on portfolio withdrawals evolve. An accredited investor in their forties with active income and diversified cash flow can withstand higher volatility than someone nearing retirement who depends on portfolio distributions. Age does not dictate risk tolerance, but it strongly influences the financial consequences of drawdowns. This distinction becomes critical when allocating to higher variance private investments.

Liquidity Needs and Distribution Planning

As investors age, liquidity transitions from a secondary concern to a core portfolio requirement. Accredited investors often hold a meaningful percentage of assets in illiquid vehicles. Age determines how aggressively those positions can be sized without impairing flexibility. Older investors typically increase exposure to private credit, income producing real assets, or shorter duration funds to support predictable distributions while maintaining diversification.

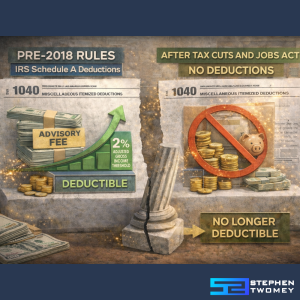

Tax Strategy and Asset Location

Age changes how tax efficiency impacts net returns. Younger accredited investors may prioritize growth and long term capital appreciation, deferring tax considerations. As investors age, tax drag becomes more visible and asset location decisions carry more weight. Strategies such as tax efficient income, timing of realizations, and coordination with estate planning tools become increasingly important. Private investments often require careful structuring to align with these goals.

Legacy Planning and Capital Intent

Later stages of life introduce questions that go beyond returns. Accredited investors begin to think more deliberately about capital intent, including philanthropy, generational wealth transfer, and governance. Age influences whether capital is optimized for maximum growth, sustainable income, or long term stewardship. Private market strategies often play a role here, offering control, alignment, and long duration exposure that supports legacy objectives.

Investment Strategies in Your 20s

The twenties represent a unique window for aggressive growth and skill building. Financial capital may be limited, but human capital is high.

Growth Focus and Career Capital

At this stage, earning power and skill development often matter more than portfolio optimization. Equity heavy portfolios make sense due to long time horizons and ongoing income.

Early Exposure to Alternatives

While access may be limited, early education around private equity and real assets builds long term strategic awareness. Small allocations through diversified vehicles can add perspective without overexposure.

Investment Strategies in Your 30s

The thirties often bring higher income, growing responsibilities, and more complex financial decisions.

Balancing Growth With Stability

Growth remains important, but diversification becomes more relevant. This is often when investors move beyond single asset portfolios.

Expanding Into Private Investments

Accredited investors may begin exploring private placements, private credit, or real estate. These assets can reduce correlation to public markets and improve risk adjusted returns. For deeper insight, see /alternative-investments.

Investment Strategies in Your 40s

The forties are a transition phase where wealth preservation becomes as important as growth.

Portfolio Diversification and Downside Risk

Sequence of returns risk becomes more relevant. Reducing reliance on public equities helps manage volatility during peak earning years.

Income Planning and Tax Efficiency

Private credit, real assets, and tax aware strategies gain importance. According to Vanguard, diversified portfolios with income components show improved drawdown resilience during market stress.

Investment Strategies in Your 50s

This decade often defines retirement readiness. Mistakes here are harder to recover from.

Capital Preservation With Growth

The goal shifts to protecting accumulated wealth while maintaining modest growth. Overly conservative portfolios risk inflation erosion.

Private Income Generating Assets

Private credit and real estate can provide predictable cash flow without full exposure to public market volatility. Liquidity planning becomes critical.

Investment Strategies in Your 60s and Beyond

Retirement does not eliminate the need for growth, but it changes priorities.

Distribution Planning and Legacy Goals

Withdrawal strategy matters as much as investment selection. Portfolios should support income needs while preserving capital for longevity.

Risk Management and Liquidity Planning

Liquidity buffers reduce the need to sell assets during market downturns. Alternative investments should be sized appropriately based on cash flow needs.

The Role of Alternative Investments Across All Ages

Alternative investments play a meaningful role in investment strategies by age because they address objectives that traditional portfolios often struggle to meet. While age influences time horizon and liquidity needs, it does not determine whether alternatives are appropriate. Instead, suitability depends on goals, risk capacity, and access. Private equity, private credit, and real assets can support growth, income, and diversification at different life stages when used deliberately. Understanding how these assets function across ages helps investors avoid the false assumption that alternatives are only for late stage wealth preservation.

Private Equity

Private equity aligns well with long term capital growth and can be relevant at multiple ages. Younger and mid career investors benefit from longer holding periods, allowing private equity to compound without the pressure of near term liquidity. For investors in their 40s and 50s, private equity can complement public equities by targeting operational value creation rather than market momentum. Even later in life, select private equity strategies focused on cash flowing businesses or shorter duration exits can play a role when properly sized. The key consideration is not age, but the ability to commit capital for extended periods and tolerate valuation opacity.

Private Credit

Private credit often becomes more attractive as investors place greater emphasis on income and downside protection. Unlike public fixed income, private credit can offer higher yields, stronger covenants, and reduced interest rate sensitivity when structured correctly. In earlier life stages, private credit can stabilize portfolios that are otherwise growth heavy. For investors approaching or in retirement, it can serve as a predictable income source that reduces reliance on public markets. Across all ages, private credit is best viewed as a risk managed income allocation rather than a substitute for speculative growth assets.

Real Assets

Real assets, including real estate, infrastructure, and energy assets, provide diversification and inflation protection across life stages. Younger investors often use real assets to balance equity volatility, while mid career investors value their role in preserving purchasing power. For older investors, income producing real assets can support cash flow needs while maintaining exposure to tangible value. Because real assets tend to have long life cycles and lower correlation to public markets, they can enhance portfolio resilience regardless of age. Liquidity and leverage risk should be evaluated carefully, especially as investors move closer to distribution phases.

Accreditation and Access Considerations

Access to alternative investments is shaped by accreditation standards, regulatory frameworks, and platform availability. The SEC accredited investor definition determines eligibility, but it does not measure sophistication or suitability. Younger high income professionals may qualify early, while older investors may qualify through net worth alone. Regardless of age, education, manager diligence, and portfolio sizing matter more than access itself. Investors should treat alternatives as strategic tools, not status symbols, and integrate them based on objectives, liquidity planning, and long term portfolio design.

Common Mistakes in Age Based Investing

Age based investing frameworks can be useful, but they are often misunderstood or applied too rigidly. Many investors rely on simplified rules that ignore personal circumstances, market conditions, and behavioral factors. The result is portfolios that look appropriate on paper but fail in practice. Below are five of the most common mistakes investors make when applying investment strategies by age.

Overreliance on Generic Age Rules

One of the most common mistakes is blindly following formulas like “100 minus your age” to determine asset allocation. These rules ignore income stability, savings rate, career risk, and personal goals. Two investors of the same age can have vastly different financial realities. Age should provide context, not dictate a fixed portfolio structure.

Confusing Risk Tolerance With Risk Capacity

Many investors assume younger people should always take more risk and older investors should avoid it. This oversimplifies reality. Risk tolerance is emotional, while risk capacity is financial. A younger investor with unstable income may have lower risk capacity than an older investor with strong cash flow and diversified assets. Failing to separate the two leads to poor decisions at every life stage.

Becoming Too Conservative Too Early

Another frequent error is reducing growth exposure too aggressively as investors enter their 40s or 50s. While capital preservation becomes more important, eliminating growth assets too soon increases the risk of falling behind inflation. Longevity risk is real, and portfolios often need growth well into retirement to remain sustainable.

Ignoring Liquidity Needs

Age based models often overlook liquidity planning. Investors may allocate to illiquid assets without considering upcoming expenses, career transitions, or retirement withdrawals. This can force asset sales during unfavorable market conditions. Liquidity should be planned intentionally, not assumed based on age alone.

Failing to Adjust as Life Changes

Age based strategies are often set once and left untouched. Major life events such as business exits, inheritance, health changes, or shifts in income require portfolio reassessment. Treating age as the primary driver instead of life stage and goals leads to outdated strategies that no longer fit the investor’s situation.

Used correctly, investment strategies by age provide structure. Used poorly, they create false confidence. The most effective approach blends age awareness with personalized planning, diversification, and ongoing review.

Final Perspective on Investment Strategies By Age

Investment strategies by age work best when combined with goal based planning and diversification. Age informs decisions, but it should never replace judgment. Thoughtful integration of traditional and alternative assets leads to more resilient portfolios.

Explore more insights on scaling businesses, building strategic partnerships, and navigating modern investment ecosystems at StephenTwomey.com.

Disclosure: None of the information on this article or site constitutes financial advice. All content is for educational purposes only.